Résumés

Abstract

We study the role of cultural distance in the choice of payment method in cross-border acquisitions. Our results based on French acquirers show that cultural distance increases the likelihood of payment in cash, which is not the case of geographical distance and linguistic difference. We also find that the most significant dimension of culture is uncertainty avoidance and that cultural distance matters most when integration of the target into the acquirer’s organizational structure is expected to be challenging. These results suggest that cash payment is a means to achieve greater control over the target, particularly when the risk of dissent is high.

Keywords:

- Acquisitions,

- cultural distance,

- payment method,

- integration,

- control

Résumé

Nous étudions l’effet de la distance culturelle sur le choix du moyen de paiement dans les fusions-acquisitions internationales. Nos résultats fondés sur un échantillon d’acquéreurs français montrent que la distance culturelle accroit la probabilité d’un paiement en espèces. Ce n’est pas le cas avec la distance géographique ni avec la distance linguistique. Nous montrons également que la dimension culturelle la plus importante est l’aversion à l’incertitude et que la distance culturelle joue un rôle plus grand lorsque l’intégration de la société cible dans la structure organisationnelle de l’acquéreur apparait plus délicate. Ces résultats indiquent que le paiement en espèces constitue le moyen de mieux contrôler la cible, notamment lorsque le risque de désaccord est important.

Mots-clés :

- Acquisitions,

- distance culturelle,

- moyen de paiement,

- intégration,

- contrôle

Resumen

Estudiamos el impacto de la distancia cultural en la elección del método de pago en las adquisiciones transfronterizas. Nuestros resultados basados en compradores franceses demuestran que la distancia cultural aumenta la probabilidad de pago en efectivo, que no es el caso de la distancia geográfica y la diferencia lingüística, mientras que el efecto de la diferencia legal se subsume en el de distancia cultural. También encontramos que la dimensión más importante de la cultura es la evitación de la incertidumbre y que la distancia cultural más importante cuando se espera que la integración de la empresa en la estructura organizacional del comprador sea un desafío. Estos resultados sugieren que el pago en efectivo es un medio para lograr un mayor control del objetivo, sobre todo cuando el riesgo de disenso es alto.

Palabras clave:

- Adquisiciones,

- distancia cultural,

- medios de pago,

- integración,

- control

Corps de l’article

A significant issue in mergers and acquisitions (M&A) is the choice of payment method. This choice has implications for the acquirer’s ownership structure and funding cost. On the one hand, cash payment is usually associated with the issue of debt, which increases the risk of financial distress. On the other hand, cash payment avoids the dilution of existing shareholders who value retaining control of the company (Amihud et al., 1990; Martin, 1996; Faccio and Masulis, 2005). Most of the discussion in the literature revolves around that tradeoff.

In this paper, we propose an alternative explanation. Cash payment is intended to assert control over the target in order to facilitate its integration within the acquirer’s organizational structure. We test this idea by looking at cross-border acquisitions performed by French firms. The hypothesis is that targets in culturally-distant markets involve greater integration challenges. The reason is that these firms are likely to have very different organizational routines as well as management and communication styles. To reduce opposition to the merger and elicit greater cooperation (Weber et al., 1996), a foreign acquirer thus needs to gain fuller control, all the more so if the target’s culture differs from its own culture.

The role of cultural distance has long been recognized in the international business literature. Kogut and Singh (1988) show that cultural differences affect the way firms expand overseas and the way they control their foreign operations. A typical pattern is to start expanding into culturally-proximate markets before venturing into culturally-distant ones. Firms also tend to set up wholly-owned subsidiaries rather than joint-ventures in culturally-distant markets (Davidson and McFetridge, 1985; Kim and Hwang, 1992; Erramilli and Rao, 1993; Beugelsdijk et al., 2018). Shane (1994), Padmanabhan and Cho (1996), and Anand and Delios (1997) argue that entry involving greater control is necessary when cultural distance is high.

Following Kogut and Singh (1988), we measure cultural distance between countries using the cultural values derived from Hofstede et al. (2010). A robustness check is performed using Schwartz’s (1999) cultural values. Our sample is based on acquisitions carried out by French firms over the period 1986-2014. We find that greater cultural distance is associated with a higher proportion of cash payment. In comparison, the effect of geographic and linguistic differences is insignificant, while the effect of legal differences is subsumed by that of cultural distance. The most significant dimension of culture is uncertainty avoidance, which describes how comfortable individuals feel under less predictable situations. Taken together, these results suggest that the objective of achieving greater integration between the acquirer and the target, which is essential to achieve operational synergies, determines the method of payment.

We further test this argument by interacting deal size, type of target, and form of acquisition with the cultural distance variable. The results show that the proportion of cash payment increases with the size of the acquisition, its structuration as a merger, and the relatedness of the acquirer to the target, but decreases for subsidiaries and private targets. This finding is in line with the idea that greater need for coordination (in larger deals) to achieve operational synergies (in related acquisitions) and greater challenges in reaching strategic agreement (in mergers) requires tighter control (as induced by a cash payment). On the other hand, this finding does not fit well with the idea that familiarity with the target’s industry (in related acquisitions), or lower frictions in access to information (for larger targets), moderates the influence of cultural distance.

Overall this study makes two contributions to the literature. First, we provide a new explanation for the choice of payment method in M&A. In addition to the concerns related to preserving the private benefits of control, posited in Amihud et al. (1990), Martin (1996), and Faccio and Masulis (2005), we highlight the issue of achieving effective control of the target, which might be resolved by choosing a cash payment. Second, we show that other widely-used measures of distance (geographic, linguistic, and legal) have no material impact on the payment method, suggesting that the informational disadvantage that they represent is not a prominent factor. In contrast, cultural distance has a significant influence because it affects the coordination process between the merging firms. Furthermore, the importance of cultural differences is underscored in the case of mergers that involve greater coordination and understanding between the two firms. In sum, cultural distance rather than other distance measures appears to be the most relevant factor when considering cross-border transactions.

The remainder of this paper is organized as follows. In the next section, we review the literature on the influence of culture on business and management practice around the world; and thus on the effect of cultural distance on the decision of a firm considering a deal with a foreign partner. We articulate the hypothesis that cultural distance increases the proportion of cash payment. We then describe the sample, the variables and the methodology. The empirical results are presented and discussed in the following section.

Literature Review and Hypothesis

We start by reviewing the concept of culture and presenting the main cultural dimensions based on the work of Hofstede (1980) and Hofstede et al. (2010). We then review the arguments and empirical evidence that link a country’s culture to its social conventions and institutions. The next section describes how foreign operations are affected by the cultural distance between the two related countries. We finally state the hypothesis that a higher proportion of cash payment is used to enforce control over a culturally-distant target.

Hofstede’s Cultural Values

Definitions of culture abound in the literature. Hofstede (1980) defines culture as “the collective programming of the mind which distinguishes the members of one human group from another”. Kluckhohn (1962) contends that culture is part of the human makeup that is learned by people “as the result of belonging to a particular group, and is that part of learned behavior that is shared by others”. More explicitly, House et al. (2004) define culture as “shared motives, values, beliefs, identities, and interpretations or meanings of significant events that result from common experiences of members of collectives that are transmitted across generations”. While they appear to be dissimilar, Tsui et al. (2007) underline the fact that all these definitions of culture are largely consistent with one another. To follow Licht et al. (2007), culture may simply represent “shared values and beliefs”.

Each country can be characterized by specific cultural values. Some countries can share common or closely related values while having opposite views regarding other values. For instance, France and Japan are both considered high risk-averse societies. However, the role of women in society is not as differentiated in France as it is in Japan. Similarly, France and Sweden both place a strong emphasis on fulfilling the individual needs of each member of society. At the same time, relations between individuals are less formalized in Sweden compared to what they are in France. Accordingly, it is essential to identify a set of cultural values that can best discriminate between the cultures of different countries.

Based on a large-scale study of IBM employees spanning a number of countries, Hofstede (1980) proposed four cultural values. We focus on his work because of its widespread acceptance and extensive use in international business studies.

Power distance is the extent to which less powerful people in a society accept the fact that power is distributed unequally. Countries high in power distance are those where hierarchical decision-making systems are more expected and accepted. In countries with low power distance, there is a preference for consultation in decision-making and less dependence on one’s supervisor.

Uncertainty avoidance is the extent to which members of society feel threatened by uncertain or unknown situations. Societies high in uncertainty avoidance tend to prefer rules and to operate in predictable situations as opposed to situations where the appropriate behaviors are not specified in advance. In these societies, people are uncomfortable with high risk and ambiguity.

Individualism (versus collectivism) refers to whether individual or collective action is the preferred way to deal with issues. In cultures oriented toward individualism, people tend to emphasize their individual needs, concerns, and interests over those of their group or organization. In individualistic cultures, individual initiative is encouraged. In collectivist societies, a person is not perceived as an individual, but derives her identity from the group to which she belongs.

Masculinity (versus femininity) refers to the degree to which values associated with stereotypes of masculinity (such as aggressiveness and dominance) and femininity (such as compassion, empathy, and emotional openness) are emphasized. High masculinity societies tend to have more sex-differentiated occupational structures with certain jobs almost entirely assigned to women and others to men. Stronger emphasis is also put on achievement, growth and challenge in one’s job.

These four initial values were later supplemented with two additional cultural values (Hofstede et al., 2010)

Long-term orientation refers to future-oriented values such as perseverance and the willingness to subordinate oneself for a purpose, to sustain efforts toward slow results, and to be parsimonious with resources. In contrast, short-term orientation refers to past- and present-oriented values such as concerns for tradition and fulfilling social obligations, and to achieve quick results.

Indulgence (versus restraint) captures the degree to which societies have strong norms regulating and suppressing the instant gratification of human needs. High indulgence societies are tolerant of basic human desires related to enjoying life and having fun. In high restraint societies, the conviction is that such gratification needs to be curbed and regulated by strict social norms.

The Influence Of Culture in Business and Management

By conditioning the interpretation of information and knowledge, culture affects beliefs, perceptions and behaviors. This suggests that culture might have a pervasive effect in business and management. In their survey, Kirkman et al. (2006) outline several areas in which culture has a direct impact (e.g. change management, negotiation, reward allocation, human resource management, leadership, etc.). Tsui et al. (2007) provide a similar discussion while Reuter (2011) discusses the influence of culture in the field of finance.

We provide a brief and personal overview of the influence of culture in economics and management.

A key area that appears to be influenced by culture is innovation. Shane (1993) shows that innovation is closely related to uncertainty acceptance, but that lack of power distance and individualism also induces high rates of innovation. One reason is that lower power distance promotes trust, which stimulates innovation. In addition, individualism emboldens managers to take actions, which has the effect of promoting innovation. Van Everdingen and Waarts (2003) indicate that all dimensions of national culture have a significant influence on the adoption of innovations. Similarly, Taylor and Wilson (2012) argue that countries with individualistic cultures are associated with higher innovation rates because of a higher demand for new technology. In contrast, collectivist values tend to slow down the rate of innovation.

Differences in innovation rates may stem from the fact that risk taking is a strong cultural trait. Hayton et al. (2002) argue that cultures that reward risk-taking and independent thinking promote radical innovation, whereas cultures that reinforce conformity and interest of the group are unlikely to exhibit risk-taking or entrepreneurial behavior. Kreiser et al. (2010) suggest that firms in countries with high uncertainty avoidance and power distance are less likely to engage in risk-taking activities. On a related note, Chen et al. (2015) find that corporate cash holdings are negatively associated with individualism and positively associated with uncertainty avoidance. Similarly, Kwok and Tadesse (2006) find that countries associated with higher uncertainty avoidance are less likely to have market-based financial systems and more likely to have bank-based financial systems, which may reflect the greater propensity of individuals to take risks.

Cultural values also appear to influence the propensity to share information. Michailova and Hutchings (2006) argue that collectivist values in China and Russia lead to intensive social relations among organizational members, which facilitate knowledge sharing between in‐group members in organizations in both countries. Chow et al. (2000) confirm that Chinese nationals share knowledge significantly less with a potential recipient who was not a member of their in-group compared to US nationals. It follows that the presentation and diffusion of information varies according to culture. Han et al. (2010) show that, in countries characterized by high individualism and low uncertainty avoidance, managers exercise more discretion in their reporting of earnings. They are also more likely to engage in earnings management. In addition, Hooghiemstra et al. (2015) show that lower uncertainty avoidance is associated with higher voluntary internal control disclosures in annual reports. In terms of communication style, Offermann and Hellmann (1997) observe that power distance is negatively associated with leader approachability while uncertainty avoidance is associated with more leader control, but lower approachability.

With regard to work-related attitudes, research indicates that the propensity to cooperate is also related to culture. Steensma et al. (2000) find that technology alliance formation by small independent manufacturers is more likely in societies that maintain cooperative values and avoid uncertainty. Bochner and Hesketh (1994) report that individuals with a collectivist background have more informal contact with fellow workers, know staff better, and are more likely to engage in teamwork. In contrast, individuals with high power distance cultural backgrounds are more task-oriented and less open with their superiors. Harrison et al. (2000) show that in countries low in collectivism and power distance, employees adapt more readily to working in different teams, or under different leaders, and are more willing to take on leadership of project teams.

The propensity to cooperate may be related to how individuals are evaluated, managed and rewarded. Wade-Benzoni et al. (2002) note that Japanese decision makers in teams use the equal allocation rule more often and expect others to be more cooperative than decision makers in US teams. Investigating how managers perceive motivation among their subordinates, DeVoe and Iyengar (2004) observe that Western managers perceive employees to be more extrinsically than intrinsically motivated, whereas Asian managers perceive their subordinates to be equally motivated by intrinsic and extrinsic factors. Cable and Judge (1994) show individual-based pay is preferred in less collectivist societies. Tosi and Greckhamer (2004) report that total CEO compensation, but also the variable portion of compensation, is positively related to individualism, while the ratio of CEO compensation to average worker compensation is positively related to power distance. Unsurprisingly, the variable portion of CEO compensation is negatively related to uncertainty aversion.

This short overview clearly highlights the importance of culture in explaining cross-country differences in practice and institutions.

The Effect of Cultural Distance in International Business

The fact that cultural disparities across countries are associated with different social and business practices implies that firms dealing with foreign partners or establishing operations overseas are likely to face significant challenges. In addition, the difficulties are expected to be greater the wider the cultural difference with the foreign partner. This explains that in their internationalization process, firms choose to expand first in countries with proximate cultures before venturing into countries with more dissimilar cultures.

Davidson (1983) argues that firms prefer entry into similar markets because it facilitates the transfer of technology and managerial resources. This also ensures a ready demand for their products and helps reduce uncertainty. Barkema et al. (1996) explain that the presence of cultural barriers punctuates an organization’s learning. Cultural distance is a prominent factor in foreign entry whenever this involves another firm, requiring both firms to engage in mutual acculturation. As an example, Delerue and Simon (2009) show that cultural differences increase the perceived relational risks in biotechnology alliance relationships. Likewise, Dodd et al. (2015) suggest that firms cross-list in markets with greater cultural similarities not only because investors are more willing to invest in culturally-familiar firms, but also because managers seek to avoid potential conflicts with culturally-disparate investors and managers.

Due to these cultural challenges, Loree and Guisinger (1995) show that the amount of foreign direct investment carried out by US firms decreases with cultural distance. Moreover, shareholder wealth is negatively impacted when firms make cross-border acquisitions in culturally-distant markets (Datta and Puia, 1995). The longevity of foreign venture (Barkema et al., 1996), the return on assets of foreign subsidiaries (Luo and Park, 2001) and the likelihood of success of foreign-owned affiliates (Li and Guisinger, 1991) are all found to decrease with cultural distance. Nonetheless, Erramilli (1991) suggests that, as their experience increases and as they become more geographically diversified, firms choose markets that are culturally less similar to their home country.

Once the decision to expand internationally has been taken, firms must choose a mode of entry. Several arrangements for organizing and conducting international business transactions are possible. For instance, firms can choose to export through independent intermediaries or they can choose to develop their own channels. Establishing foreign operations may involve either greenfield investment or the acquisition of an existing firm. The advantage of greenfields is that the firm is able to organize the operations in its favorite way. The disadvantage is that setting up the operations takes time and the firm may not be able to immediately produce goods and services. In contrast, acquisitions provide assets that are already in place and ready to service customers. However, the drawback is that the acquired organization may not fit the acquirer’s culture.

As a result, the choice between an acquisition and a greenfield is found to depend on the cultural distance of the two countries. The greater the cultural distance, the more challenging and costly the integration of the target. The obvious reason is that the two firms are likely to have radically different organizational and managerial practices as well as communication styles (as indicated in the previous section). Hence, the less likely the choice of an acquisition. Despite the associated delay, the choice of greenfield can be justified on the grounds that the risks and afferent costs of forming a team with a vastly different culture are lower.

Shane (1994) finds that cultural differences in trust affect the perception of transaction costs and the preference for foreign direct investment across countries. Drogendijk and Slangen (2006) document that large cultural distance significantly increases the likelihood that Dutch multinational firms choose greenfields over acquisitions. Harzing (2002) confirms that the tendency to choose greenfield over acquisition increases with cultural distance. Similarly, firms display a tendency to choose a joint venture over an acquisition (Kogut and Singh, 1988; Chang and Rosenzweig, 2001; Beugelsdijk et al., 2018) as the cultural distance between countries increases.

When going for an acquisition, a key issue is the degree of control over the target. Greater control is assumed to be necessary for culturally-distant targets in order to achieve the expected synergies. Accordingly, cultural distance tends to involve higher control entry modes. This result is consistent with the idea posited by Anderson and Gatignon (1986) that this is the optimal way to transfer technology and management practices to a very different cultural environment. As a matter of fact, Weber et al. (1996) show that the greater the cultural distance between the merging firms, the greater the stress, the more negative the attitudes towards the merger, and the lower the staff cooperation. Full ownership also offers the possibility of dismissing the target management teams more easily, in case of disagreement with the strategy of the acquiring firm (Gaur and Lu, 2007). More generally, cultural distance problems are considered to be better addressed with strong hierarchical control.

Consistent with the above arguments, Shane (1994), Padmanabhan and Cho (1996) and Anand and Delios (1997) show that greater cultural distance is associated with higher control entry modes. Focusing on the case of US manufacturing firms investing abroad, Shane (1994) finds that higher equity stakes, a proxy for tighter control, is used when cultural distance is large. Padmanabhan and Cho (1996) examine the foreign entry mode of Japanese manufacturers and find that they are more likely to set up wholly-owned subsidiaries in culturally-distant countries. Erramilli, Agarwal, and Kim (1997) do the same with Korean firms and also conclude that large cultural distance is associated with higher-equity modes of entry.

Also indicative of the challenges and need to ensure greater control over culturally-distant managers, Roth and O’Donnell (1996) show that a higher proportion of incentive-based compensation is used for the managers of subsidiaries located in culturally-distant countries. The fact that firms undertake less R&D in culturally-distant countries also reveals the difficulty of controlling employee behavior in culturally-distant firms (Richards and De Carolis, 2003).

Cultural Distance and Payment Method in Foreign Acquisitions

Mergers and acquisitions (M&A) is an area that is most likely to be affected by cultural distance. Ahern et al. (2015) show that cultural distance affects merger volume and synergy gains. More precisely, the volume of cross-border mergers is significantly lower when countries are culturally distant. In addition, greater cultural distance in trust and individualism leads to lower combined announcement returns, suggesting lower synergy gains. Reus and Lamont (2009) explain that cultural distance impedes the understandability of key capabilities that need to be transferred and constrains communication between acquirers and their acquired units. Likewise, Stahl and Voigt (2008) point out that cultural difference can create major obstacles to achieving integration benefits.

In order to achieve the expected synergies from the merger, greater control over the target is required. Reus and Lamont (2009) argue that strong integration allows learning opportunities arising in international acquisition to be exploited; and increases capabilities and performance. Acquirers that can overcome the impeding effects of cultural distance on understanding key capabilities and effective communication are likely to reap significant performance gains. Bresman et al. (2010) show that the immediate post-acquisition period is characterized by imposed one-way transfers of knowledge from the acquirer to the acquired. High-quality reciprocal knowledge transfers only arise gradually afterwards.

Accordingly, a greater proportion of cash payment is expected for more culturally-distant targets. This enables the acquiring firm to achieve higher ownership concentration and therefore to enforce its organizational standards. As Anderson and Gatignon (1986) suggest, this might be the best way to transfer technology and management practices to a very different cultural environment. This may also reduce opposition to the deal and mitigate the risk of failure often seen in mergers. By gaining greater control over the target, the acquiring firm may more easily dismiss the target’s management or threaten to do so (Gaur and Lu, 2007), which ensures greater cooperation (Weber et al., 1996). The following hypothesis stems directly from this need for greater control.

Hypothesis: The proportion of cash payment in cross-border acquisitions is positively related to the cultural distance between the acquirer and the target.

Data and Methodology

Sample

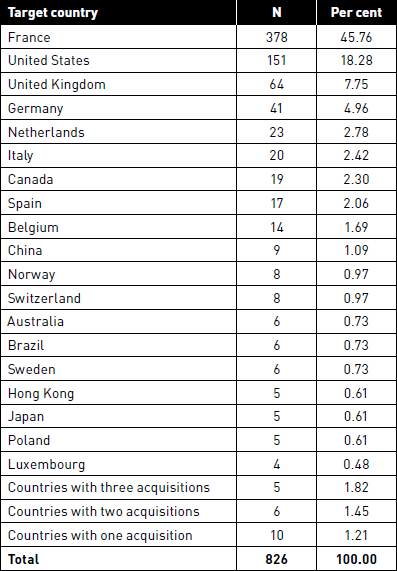

We use Thomson Reuters SDC Global Mergers & Acquisitions database to construct our sample. We begin by selecting all acquisitions by French firms for the period from January 1986 to April 2014 with a minimum value of €1 million. Listed as well as private acquirers are included. Transactions for which the method of payment is missing are eliminated. We also drop deals in which the target is already controlled by the acquirer and in which the acquirer does not seek to achieve majority control. Likewise, deals for which the target is located in a country not covered by Hofstede (1980) are dropped. The final sample consists of 826 acquisitions of which 378 (45.76%) involve a French target and 448 (54.24%) concern a foreign target.

Figure 1 shows the distribution of the sample over time. While the number of transactions appears to increase as time passes, it also displays significant year-on-year fluctuations. A large number of acquisitions cluster around the late 1990s and appear to be encouraged by the strong market conditions surrounding the internet bubble. Another smaller peak takes place in the period leading up to the 2008 global financial crisis.

FIGURE 1

Number of acquisitions by year

Table 1 presents the distribution of targets by country. Domestic acquisitions represent 45.76% of the sample. The most frequent countries for foreign acquisitions are the US (18.28%), the UK (7.75%) and Germany (4.96%). As it turns out, the overwhelming majority of foreign targets are located in developed economies. Very few are in Asia. Targets in China represent about 1.1% of the sample and those in Japan and in Hong Kong only 0.6%.

Main Variables

In line with Faccio and Masulis (2005), the dependent variable is the proportion of cash payment. This figure comprised between 0 and 100% is directly retrieved from SDC.

The main explanatory variable, Hofstede cultural distance, is measured as in Kogut and Singh (1988) using Hofstede et al.’s (2010) cultural values. In effect, it represents the average squared difference between the target country and the acquirer country (France) in each of Hofstede et al.’s (2010) cultural dimensions, which is standardized by the index’s variance across countries.

The variable I represents one of Hofstede et al.’s (2010) six cultural values. The index j thus varies from 1 to 6. The indices k and F denote the target country and the acquirer country (France), respectively.

Table 1

Distribution of acquisitions by target country

To investigate the role of each cultural dimension, we use the relevant term under the summation.

An alternative measure of cultural distance is based on the work of Schwartz (1999). The latter proposed a systematic identification of 54 individual values recognized across cultures, which were then reduced to a set of seven meaningful and interpretable dimensions along which national cultures are found to differ. Conservatism represents a culture’s emphasis on maintaining the status quo, propriety, and restraining actions or desires that may disrupt the solidarity of the group or the traditional order. Intellectual autonomy refers to the extent to which people are free to independently pursue their own ideas and intellectual directions. Affective autonomy refers to the extent to which people pursue their affective desires. Hierarchy denotes the extent to which it is legitimate to distribute power, roles and resources unequally. Egalitarian commitment refers to the extent to which people are inclined to voluntarily put aside selfish interests to promote the welfare of others. Mastery expresses the importance of getting ahead by being self-assertive. Harmony denotes the importance of fitting harmoniously into the environment (Schwartz, 1999).

A similar indicator of distance is constructed using these seven cultural dimensions.

We compare the effect of cultural distance with three widely-used measures of distance

Geographical distance is the number of kilometers between the capitals of the acquirer’s country and that of the target. A log transformation is applied to that measure. Chevalier and Redor (2010) find that US acquirers use more cash to purchase foreign targets. The argument is that investors (on the target’s side) are less likely to hold shares in geographically distant firms (Grinblatt and Keloharju, 2001).

Linguistic difference is a dummy variable that takes the value of 0 if the target’s country shares the same language as the acquirer’s country (i.e. French); and 1 if the target’s country uses a different language. The argument is that linguistic differences increase the cost of obtaining information regarding foreign firms. In line with this argument, Chevalier and Redor (2010) find that US acquirers use less cash to pay for targets in English-speaking countries.

Legal difference is a dummy variable that takes the value of 0 if the target’s country has a civil law system as in France; and 1 if it operates under common law. The legal system is often viewed as a strong reflection of a country’s cultural values. As a matter of fact, cultural distance tends to be lower when two countries share the same legal origin.

Control Variables

We follow the literature in selecting the relevant control variables for the method of payment.

Deal value. Large acquisitions are associated with a higher probability of stock payment (or lower probability of cash payment). The rationale is that stock payment enables the risk of adverse selection to be shared with the target (Hansen, 1987). Evidence on the negative influence of deal value can be found in Martin (1996), and Ghosh and Ruland (1998).

Acquirer size. Large acquirers are more likely to pay in cash. The reason derives from their lower bankruptcy costs and better access to debt financing (Faccio and Masulis, 2005).

Acquirer leverage. The payment method should be chosen to optimize the acquirer’s post-acquisition capital structure. The higher its leverage, the less likely it is to use a payment in cash (Faccio and Masulis, 2005). Conversely, acquirers with unused debt capacity (or excess cash) are more likely to pay in cash (Martin, 1996; Karampatsas et al., 2014). Furthermore, Murphy and Nathan (1989) show that announcement returns are positive if the payment method helps the acquirer to move towards its optimal capital structure.

Acquirer profitability. Higher profitability should induce a higher probability of paying in cash. Moreover, the pecking order model suggests that profitable firms have greater debt capacity.

Acquirer listing status. Publicly-listed acquirers have the obvious advantage of being able to offer liquid shares as currency. All other things being equal, they are less likely to pay in cash.

Target status. We distinguish private firms and subsidiaries from listed firms using two dummies. Faccio and Masulis (2005) argue that corporate owners are more likely to ask for a payment in cash. In the case of private firms, ownership is typically concentrated, implying more effective governance and better performance. Stock payment enables the target’s owners to maintain significant ownership over the combined firm, which should benefit the acquirer. Indeed, Chang (1998) reports that acquirers of private targets achieve higher returns if the latter are paid in stock.

Relatedness. Target shareholders are more likely to accept stock payment from acquirers in the same industry. This is justified by their greater familiarity with risk and the prospects of that industry (Faccio and Masulis, 2005). Redor (2007) observes that the likelihood of stock payment is higher for related acquisitions.

Structure of transaction. Acquisitions in the form of a merger are usually paid for in stock; while tender offers are typically paid in cash.

Indicator for booming markets. The volume of acquisitions is correlated with favorable market conditions. Due to fierce competition for targets, buyers are likely to offer cash in order to speed up the transaction.

Industry dummies are included to capture any industry-specific factor that may affect the payment method.

Methodology

The proportion of cash used as payment method is explained by an indicator of cultural distance and the usual variables influencing the mode of payment in cross-border acquisitions. Since the dependent variable takes a value between 0 and 1, with strong clustering at the edge, we perform Tobit regressions as in Faccio and Masulis (2005) with a lower limit at 0 and an upper limit at 1. The direct effect of cultural distance is thus assessed by running the following regression:

To investigate whether the effect is moderated by expected post-acquisition difficulties, we add an interaction term with the moderating variable. Note that the moderating variable is already in the list of control variables and is therefore not explicitly indicated.

The variables suggesting greater integration problems are:

Merger: this form of business combination requires an agreement between the boards of each company. In effect, it gives veto power to the target’s management. Cultural differences are thus expected to make the prospect of an agreement more challenging.

Deal size: larger acquisitions involve more difficult integration problems that will be compounded by dealing with culturally-distant managers.

Related acquisitions: While related acquisitions tend to create more value, they also pose greater integration problems. One reason is that each firm may have its own way of doing the same thing. As a result, having to adapt to the acquirer’s specific processes is likely to involve a lot more resentment and resistance among the managers and staff of the target.

Target status: Listed targets lose their independence after being acquired. Their managers are thus likely to exhibit greater resistance to the acquirer’s directives. In contrast, subsidiaries simply swap one controlling shareholder for another, and are unlikely to pose specific challenges. Likewise, the managers of private firms are typically acquainted with a tight control and should not oppose the instructions of their new owners.

Empirical Results

Descriptive Statistics

Table 2 presents the descriptive statistics for the sample. Panel A shows that cash is the favorite payment method with an average proportion of cash payment around 69% and more than half of all transactions entirely paid in cash. Stock payment is also common with an average proportion of 26.6% in all payments. Panel B indicates that about 41.8% of all acquisitions are structured as mergers, while 58.2% take the form of tender offers. About 69% of deals are related in the sense that they involve an acquirer and a target in the same industry. Almost 95% of acquirers are publicly-listed firms, but nearly 30% of targets are private firms, and 34% are subsidiaries, and the remaining 36% are publicly-listed firms. While the boom indicator covers only 10 years (1996-2000 and 2003-2007) it concerns well over half of the acquisitions since the latter tend to take place during the good years.

Panel C describes the Hofstede and Schwartz cultural distance variables as well as three other distance variables. Although 54.3% of the targets are foreign, only 48.9% involve a language that is not French since some targets are located in French-speaking countries. Panel D provides the distance between France and the target country for each of the six cultural dimensions of Hofstede (2010). Panel E does the same for each of the seven cultural dimensions of Schwartz (1999). While all these variables are standardized, it is possible to notice that their mean values are quite different. For example, the average distance based on power distance is quite high since France scores relatively high on that cultural dimension, and is thus distant from other target countries whose score is lower. In comparison, the average distance based on individualism is much lower since France can be characterized as an average country on that cultural dimension.

Table 3 displays the pairwise correlation between the variables. Larger deals and mergers tend to involve a lower proportion of cash payment as in Faccio and Masulis (2005). In contrast, larger and more profitable acquirers are more likely to pay in cash. Interestingly, acquirers are less likely to use cash during boom years. Consistent with our hypothesis, greater cultural distance is also associated with a higher proportion of cash payment. Among the other notable correlations, larger acquirers are associated with larger targets. Larger acquirers are also less likely to target a private firm, probably due to the latter’s smaller size. But foreign acquisitions are likely to involve a larger acquirer. Finally, the two lines at the bottom show that targets in culturally-distant countries are more likely to be paid in cash; and also more likely to involve a larger acquirer. These results might have been expected since larger firms are more likely to have foreign operations.

Table 2

Descriptive statistics for the sample

See Appendix 1 for definition of the variables

Table 3

Correlation between the variables

* indicates significance at the 1% level

Cultural distance as Determinant of Payment Method

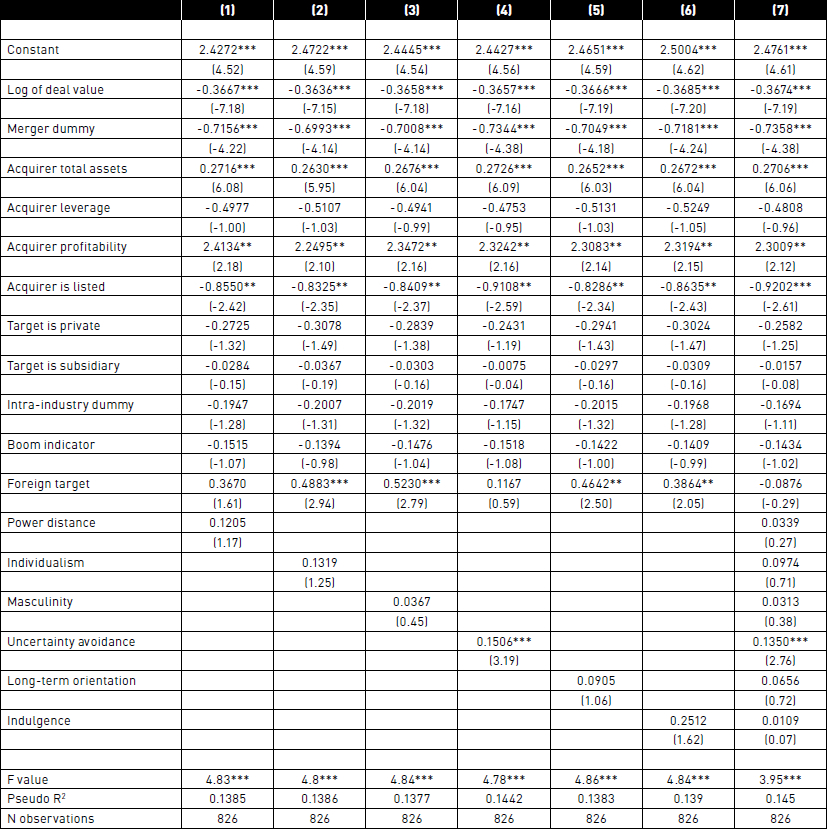

Table 4 presents the results of Tobit regressions explaining the proportion of cash payment. Before turning our attention to the distance variables, we quickly review the influence of the usual explanatory variables of payment method.

The negative coefficient on deal value indicates that larger transactions are associated with a lower proportion of cash payment, consistent with the greater need for the risk of adverse selection to be shared with the target’s shareholders. At the same time, the positive coefficient on acquirer size indicates that larger acquirers are more likely to pay in cash. This result is consistent with the argument that external financing is easier for large firms, since larger firms are more diversified, have lower issue costs, and have better access to debt financing. In line with Faccio and Masulis (2005), the combination of the two coefficients implies that the probability of a cash payment decreases as the relative size of the transaction increases.

Table 4

Regressions of Cash Payment Using Hofstede Cultural and Other Distance Variables

The t-ratios between brackets are based on robust standard errors. ***. **. * indicate significance at the 1%, 5%, and 10% level.

More profitable acquirers are more likely to use cash payment. Their higher profitability may help them to replenish their cash balances over time and facilitates their access to debt financing. Profitable acquirers may also be reluctant to share their value with the target’s shareholders. On the other hand, the acquirer’s leverage has an insignificant influence on the mode of payment. This finding differs from Faccio and Masulis (2005), who argue that highly leveraged firms are less likely to use cash since this increases the likelihood of financial distress. The decision to structure the acquisition in the form of a merger instead of a tender offer is associated with a lower probability of cash payment. This finding is consistent with Fishman’s (1989) model of competitive bidding, but not with Martin (1996), who documents a lower probability of stock financing in tender offers. As expected, listed acquirers are less likely to offer cash as payment since their shares benefit from higher liquidity.

The status of the target has no significant influence on the method of payment. Contrary to our expectation, related acquisitions are not associated with a higher probability of stock payment. While lower information asymmetry may facilitate the evaluation of the target, reducing the need for sharing the risk of adverse selection, cash payment confers greater control over the target, thus helping the acquirer to realize operating synergies. Finally, the negative correlation between cash payment and boom years disappears when other variables are taken into account.

The Hofstede cultural distance variable in Model 1 has a highly significant effect with the expected positive sign. More precisely, targets located in countries that are more culturally-distant from the acquirer’s country are more likely to be paid in cash. This finding is in contrast to the result in Chevalier and Redor (2010), where US acquirers are less likely to pay culturally-distant targets using cash. This result can be explained by the need for the acquirer to exert greater control over the target given the more challenging integration issues that are likely to crop up given the widely different cultures of the two firms.

In Model 2, we use the (log of) geographical distance between the acquirer’s and the target’s capital cities. The reasoning is that the larger the distance, the greater the information asymmetry; and hence, the higher the likelihood of a cash payment. We find that while the coefficient is positive, it is not significant. This result is also in contrast to the significant role of geographical distance for US acquirers documented in Chevalier and Redor (2010). A possible explanation might be that geographical distance adds an extra layer of uncertainty in the case of US acquirers, but not in the case of French acquirers.

In Model 3, we use an indicator for difference in language and find that the effect is also insignificant. This result indicates that targets from a non-French speaking country are as likely to be paid in shares as targets from a French-speaking country. This result is again in contrast to the case of US acquirers, which are more likely to pay their foreign acquisitions in shares if they are located in another English-speaking country (Chevalier and Redor, 2010).

Model 4 shows that targets in a common-law country are more likely to be paid in cash. This finding indicates that acquirers are more inclined to use cash when they do not share the same legal system with the target, which is congruent with higher informational costs. Since the legal system tends to go alongside the cultural traits of a country, and since the legal system is a significant determinant of the method of payment, one concern could be that the cultural distance variable is actually capturing the difference in legal system between the acquirer and the target’s countries. To evaluate this possibility, we include both variables in Model 5. The effect of cultural distance is then slightly weaker, but remains significant at the 5% level, thus indicating that the impact of cultural distance is not subsumed by a difference in legal system. Quite the opposite, it appears that the effect of a difference in legal system is entirely explained by the role of cultural distance.

Overall, the results in Table 4 reveal a role for cultural distance that is distinct from the effect that geographical distance, and language and legal differences, might have. While differences in language and large geographical distances are likely to induce greater information asymmetry, implying larger acquisition costs, they do not appear to have a significant influence on the mode of payment. In contrast, the significant influence of cultural distance may be explained by control and coordination issues between the merging firms. Reaching agreement in the deployment of strategy and achieving operational synergies are more difficult between boards with different cultural backgrounds. Since stock payment offers a greater role for the target’s managers, it poses greater cultural challenges, and presents a higher risk to the success of a merger. It follows that acquirers have greater incentives to pay culturally-distant targets using cash in order to achieve greater control. This result is consistent with the choice of greenfields over acquisitions when firms expand overseas and their need to control more tightly foreign subsidiaries located in culturally-distant countries.

Do all Dimensions of Culture Matter?

Having established the influence of culture on the payment decision, our next step is to check whether each dimension of culture is equally important. For that, we use the distance between the target’s and the acquirer’s countries on each cultural dimension. To facilitate the comparison of the regression coefficients, the squared differences are normalized as in Kogut and Singh (1988). Table 5 displays the Tobit regression results. Interestingly, the coefficients on all the distance variables in Models 1-6 are positive, indicating that greater distance is consistently associated with a higher probability of a cash payment.

To interpret the results, it may be convenient to consider a US or UK firm as the target since both countries are culturally distinct from France. Besides, the US and the UK are also the countries with the largest number of targets outside of France. Cultural traits in the US and the UK are similar in every dimension, while being very different from French cultural traits. For instance, they both score very high on the individualism scale, and very low on the power distance scale, while France scores much lower on individualism and relatively high on power distance. The only caveat is that, relative to the US, the UK appears to be less distant from France in terms of long-term orientation.

With this in mind, we observe in Models 1-6 that targets located in a country, like the US or the UK, with lower power distance, higher individualism, high masculinity, lower uncertainty avoidance, lower long-term orientation, and higher indulgence, are more likely to be paid in cash. While France differs quite significantly from the US and the UK on all dimensions, only the distance related to uncertainty avoidance turns out to be highly significant. Moreover, when all the variables are included in Model 7, it is the only variable that retains a significant influence.

Given the high level of uncertainty avoidance that is characteristic of France, the result indicates that cash is more likely to be used when the target is in a country with a low level of uncertainty avoidance. Since uncertainty avoidance pertains to how comfortable people feel with uncertainty and ambiguity, what they expect in terms of beliefs and behavior, how important practice is relative to principles, etc., these differences are likely to present considerable challenges towards achieving effective integration of the target, especially if the target is given a substantial voice in future decision-making. For instance, the acquirer may have precise objectives and more rigid procedures for conducting business and running operations; it may not value flexibility as much and may be less tolerant of deviations from expected practice; it may also have more centralized decision-making and may leave little discretion to local managers. This may not go down well with managers accustomed to having greater decision-making power, and who are entrusted in their appreciation of problems, and authorized to take immediate actions.

Table 5

Regressions of cash payment using each of Hofstede’s cultural dimensions

The t-ratios between brackets are based on robust standard errors. ***. **. * indicate significance at the 1%, 5% and 10% level.

Stock payment implies that the target’s owners will continue to share responsibility in the joint business. Hence, their opinion on how the business should be run cannot be ignored. That will raise considerable challenges if their behaviors and expectations are substantially different from those of the acquirer. In contrast, cash payment entails that the target’s owners will be exiting the business. Accordingly, the target’s managers will have new owners to whom they are accountable. There is thus greater expectation to behave according to the acquirer’s procedures and business culture, which should facilitate the target’s integration into the acquiring firm. This may explain why the method of payment is so strongly associated with cultural distance.

When Does Cultural Distance Matter Most?

While the effect of culture on payment decisions appears to be firmly established, we also want to understand whether the role of cultural distance is more significant in specific circumstances. More precisely, when post-acquisition integration is expected to be more challenging, is cultural distance likely to play a bigger role? With that in mind, we focus on the size of the acquisition (deal value), the type of target (private firms and subsidiaries versus public firms), its relatedness with the acquirer (being in the same versus being in a different industry) and the structure of the transaction (mergers versus tender offers). Table 6 presents the results of Tobit regressions in which each of these variables is interacted with the Hofstede cultural distance.

Table 6

Analyzing the moderating effect of expected post-acquisition integration difficulty

The t-ratios between brackets are based on robust standard errors. ***. **. * indicate significance at the 1%, 5%, and 10% level

In Model 1, we test the argument that targets located in countries that are more culturally distant present greater integration challenges the larger they are; hence, the more likely they are to be paid in cash. The positive coefficient on the interaction term, log deal value × cultural distance, is consistent with that prediction. As a matter of fact, larger targets are expected to play a greater and more active role in the combined firm. Moreover, their beliefs and deep-seated attitudes are unlikely to be diluted in the acquirer’s culture if they also own a substantial stake in the combined firm (after receiving shares as payment). Accordingly, the use of cash as payment method appears to be the way to deal with that ambiguity and makes clear whose rules are to be followed in the merged entity.

In Model 2, we then interact the cultural distance variable with the merger dummy. In mergers, the acquirer and the target’s board reach an agreement that is put to the vote of shareholders. Cultural closeness is thus paramount in facilitating the negotiation process, especially regarding the strategy to follow, the procedures to put in place, and the role of the senior executives of each firm in the new business entity. Hence, the greater the cultural distance, the harder it will be to find a common ground; and the higher the likelihood that the acquirer will choose to pay in cash. The empirical result strongly supports this argument.

The next column examines the moderating role of firm relatedness on the effect of cultural distance. For a target in the same industry, rivalry is likely to be intense. Senior executives are likely to have similar expertise and credentials. Attribution of roles in the combined firm thus requires a fine understanding of each executive’s capabilities. This necessary step toward setting up the organizational structure post-acquisition is quite delicate and is likely to hit a nerve, the greater the cultural distance between the two firms. Hence, cash payment might be a means to clear the obstacles by putting the acquirer more directly in charge of the combined firm. The result in Column 3 indicates that, while cultural distance positively affects the likelihood of a cash payment for an unrelated target (with the coefficient on cultural distance being positive and significant), its effect for a related target is significantly higher (with the coefficient on the interaction term, intra industry × cultural distance, also being positive and significant).

In contrast, Model 4 reveals that the coefficients on the interaction terms with the target’s private dummy and subsidiary dummy are significantly negative. This result is consistent with the idea that private firms are easier to take over. It explains why the announcement of a private firm acquisition is associated with higher buyer abnormal returns (Chang, 1998; Fuller et al., 2002; Faccio et al., 2006). One contributing factor is that private targets are typically smaller relative to the acquirer, which is confirmed by the highly negative correlation between private dummy and acquirer’s size (correlation = –32%). This difference in size reduces the incidence of conflicts related to management control in the merged company. Accordingly, cultural differences are less likely to become serious obstacles, resulting in a lesser need to use cash. Similarly, subsidiaries are already under the control of a larger firm. Transfer of control is thus unlikely to present a specific challenge to the new owner. In addition, corporate owners are likely to prefer cash that they can use in other projects rather than receiving shares (Faccio and Masulis, 2005).

Overall, the results underscore the fact that cultural distance is a highly significant factor in the process of carrying out a foreign acquisition that requires an adaptation of the method of payment. The idea that culturally- distant targets present greater challenges and that payment in cash serves to resolve trickier negotiations and facilitates control over the combined entity is validated using the whole sample. But we also show that specific (larger, related, or publicly-listed) targets or transactions (merger versus tender offer) compound the challenges associated with the acquisition of culturally-distant targets. These results confirm the role of cultural distance as a barrier to the combination of separate firms. Method of payment appears to serve as an effective mechanism for allocating control rights in the post-acquisition firm. When dispersion of control is likely to pose greater challenges, due to differences in behavior and expectations, it seems optimal to concentrate this control in the hands of the acquiring shareholders. Hence, the greater prevalence of cash payments observed in such cases.

Robustness Check Using Schwartz Cultural Values

In Table 7 we test the robustness of our findings by substituting Schwartz’s (1999) cultural values for those of Hofstede (2010). Both cultural distance variables are highly correlated with a correlation coefficient of over 0.89. Nonetheless, Model 1 shows that cultural distance based on Schwartz has a positive but insignificant influence on the proportion of cash payment. This might suggest that Hofstede’s cultural values are better able to capture how differences in culture affect the choice of payment method in foreign acquisitions. The absence of a significant effect does not imply, however, that Schwartz’s cultural values inadequately capture cultural difference. They may simply be less precise. Drogendijk and Slangen (2006) similarly find that Hofstede’s cultural values better explain entry mode by Dutch multinationals compared to Schwartz’s cultural values.

We then interact Schwartz’s cultural distance with the contextual variables used in Table 6. Model 3 suggests that larger acquisitions raise similar concerns in the acquirer’s mind. More distant targets will be more likely to be acquired in cash to overcome potential resistance and ensure greater control over the target. Model 4 indicates that cultural distance plays a greater role in mergers as opposed to tender offers. Although assessed quite differently, cultural distance appears to be of similar concern to the acquirer and prompts the latter to choose cash payment in the takeover of more culturally-distant targets. Model 6 indicates that private firms and subsidiaries present less of a challenge in culturally-distant countries. The only insignificant result is for intra-industry (related) acquisitions, which is weakly significant, using Hofstede’s cultural values.

Overall, the results confirm the role of cultural distance in the setting up and in the management of foreign operations. Because they anticipate greater challenges in the integration of a culturally-distant target and because they are confronted with greater difficulty in the negotiation process, acquirers choose to offer cash as payment to speed up the transaction and ensure greater control. Although constructed in a different manner, Schwartz’s cultural values appear to capture essentially the same difference in beliefs that is likely to influence the success of a foreign acquisition.

Conclusion

This paper examines the influence of cultural distance on the choice of payment method for foreign acquisitions. Faccio and Masulis (2005) find that European firms are more likely to use cash to buy a foreign target. We extend their results using a sample of French acquirers over the period 1986-2014. We show that cultural distance increases the likelihood that the target is paid in cash. A standard explanation is that foreign targets discount a stock offer due to the greater information asymmetry associated with distance; thus giving the acquirer an incentive to pay in cash. However, we find no evidence that geographical distance and language difference have an influence on the method of payment; while the effect of legal distance is subsumed by that of cultural distance.

Although all dimensions of culture are highly correlated, only uncertainty avoidance is found to be statistically significant. French acquirers appear to treat targets in countries characterized by lower levels of uncertainty avoidance with an extra degree of caution, which is reflected in a greater incidence of cash payments. This finding suggests that French acquirers are concerned that the less formal behavior of the target’s managers and their more outspoken style may clash with more rigid French conventions. Using cash payment enables the acquirer to better control the target through the exit of its previous owners. This line of explanation is consistent with the tendency to choose greenfields over acquisitions, or larger ownership stakes in joint ventures, when firms expand overseas (Anand and Delios, 1997; Padmanabhan and Cho, 1996; Harzing, 2002; Erramilli et al., 1997).

Table 7

Regressions of cash payment using Schwartz cultural distance

The t-ratios between brackets are based on robust standard errors. ***. **. * indicate significance at the 1%, 5%, and 10% level.

We test this explanation by interacting cultural distance with variables suggesting the potential for greater post-acquisition integration problems. The results show that the relation between cash payment and cultural distance is stronger when the acquisition can be expected to be more problematic, but weaker when fewer issues are expected. More specifically, in larger deals in the same industry, having a similar culture appears to help contain the inherent conflicts regarding the firm’s strategy. In contrast, greater cultural distance is likely to increase the risk of conflicts. Hence, the greater incentive to buy out the target’s owners by offering them cash.

We achieve similar results using Schwartz cultural items. However, the direct effect is weak and is only significant for acquisitions that are expected to generate greater post-acquisition problems. Overall, the study provides another indication that cultural factors affect a firm’s choice in its international operations. There are, nonetheless, several limitations to our work. The first is that the results are taken from the perspective of French firms. An obvious extension would thus be to carry the test to a larger sample of acquirers from different countries. Another extension would be to investigate more precisely how cultural differences affect the management of acquired firms. Clinical studies might provide unique and invaluable insights in this respect.

Parties annexes

Appendix

appendix 1. Description of variables

Biographical notes

Pascal Nguyen is a professor of corporate finance and a former dean for faculty and research at ESDES Business School. He is currently a visiting professor at Hitotsubashi University. He was previously affiliated with NEOMA Business School, the University of Technology Sydney and the University of New South Wales. His research interests are in corporate governance and social responsibility. He publishes regularly on these issues in various international journals.

Samia Belaounia holds a PhD in management from Paris Dauphine University. She is currently an Associate Professor at Neoma Business School. Her main research interests are internationalization strategies and the determinants of corporate financial policies. She has published in refereed journals such as Finance Contrôle Stratégie and Revue Française de Gestion. She is a reviewer for International Business Review.

Bibliography

- Ahern, Kenneth R.; Daminelli, Daniele; Fracassi, Cesare (2015). “Lost in translation? The effect of cultural values on mergers around the world”, Journal of Financial Economics, Vol. 117, p. 165-189.

- Amihud, Yakov; Lev, Baruch; Travlos, Nickolaos G. (1990). “Corporate control and the choice of investment financing: The case of corporate acquisitions”, Journal of Finance, Vol. 45, p. 603-616.

- Anand, Jaideep; Delios, Andrew (1997). “Location specificity and the transferability of downstream assets to foreign subsidiaries”, Journal of International Business Studies, Vol. 28, p. 579-603.

- Anderson, Erin; Gatignon, Hubert (1986). “Modes of foreign entry: A transaction cost analysis and propositions”, Journal of International Business Studies, Vol. 17, p. 1-26.

- Barkema, Harry G.; Bell, John H. J.; Pennings, Johannes M. (1996). “Foreign entry, cultural barriers, and learning”, Strategic Management Journal, Vol. 17, p. 151-166.

- Barkema, Harry G; Shenkar, Oded; Vermeulen, Freek; Bell, John H. J. (1997). “Working abroad, working with others: How firms learn to operate international joint ventures”, Academy of Management Journal, Vol. 40, p. 426-442.

- Beugelsdijk, Sjoerd; Kostova, Tatiana; Kunst, Vincent E., Spadafora, Ettore; van Essen, Marc (2018). “Cultural distance and firm internationalization: A meta-analytical review and theoretical implications”, Journal of Management, Vol. 44, p. 89-130.

- Bochner, Stephen; Hesketh, Beryl (1994). “Power distance, individualism/collectivism, and job-related attitudes in a culturally diverse work group”, Journal of Cross-Cultural Psychology, Vol. 25, p. 233-257.

- Bresman, Henrik; Birkinshaw, Julian; Nobel, Robert (2010). “Knowledge transfer in international acquisitions”, Journal of International Business Studies, Vol. 41, p. 5-20.

- Cable, Daniel M.; Judge, Timothy A. (1994). “Pay preferences and job search decisions: A person‐organization fit perspective”, Personnel Psychology, Vol. 47, p. 317-348.

- Chang, Saeyoung (1998). “Takeovers of privately held targets, methods of payment, and bidder returns”, Journal of Finance, Vol. 53, p. 773-784.

- Chang, Sea‐Jin; Rosenzweig, Philip M. (2001). “The choice of entry mode in sequential foreign direct investment”, Strategic Management Journal, Vol. 22, p. 747-776.

- Chen, Yangyang; Dou, Paul Y.; Rhee, S. Ghon; Truong, Cameron; Veeraraghavan, Madhu (2015). “National culture and corporate cash holdings around the world”, Journal of Banking & Finance, Vol. 50, p. 1-18.

- Chevalier, Alain; Redor, Etienne (2010). “The determinants of payment method choice in cross-border acquisition”, Bankers, Markets and Investors, Vol. 106, p. 4-14.

- Chow, Chee W.; Deng, F. Johnny; Ho Joanna L. (2000). “The openness of knowledge sharing within organizations: A comparative study of the United States and the People’s Republic of China”, Journal of Management Accounting Research, Vol. 12, p. 65-95.

- Datta, Deepak K.; Puia, George (1995). “Cross-border acquisitions: An examination of the influence of relatedness and cultural fit on shareholder value creation in US acquiring firms”, MIR: Management International Review, Vol. 35, p. 337-359.

- Davidson, William H. (1983). “Structure and performance in international technology transfer”, Journal of Management Studies, Vol. 20, p. 453-465.

- Davidson, William H., McFetridge, Donald G. (1985). “Key characteristics in the choice of international technology transfer mode”, Journal of International Business Studies, Vol. 16, p. 5-21.

- Delerue, Hélène; Simon, Eric (2009). “National cultural values and the perceived relational risks in biotechnology alliance relationships”, International Business Review, Vol. 18, p. 14-25.

- DeVoe, Sanford E.; Iyengar, Sheena S. (2004). “Managers’ theories of subordinates: A cross-cultural examination of manager perceptions of motivation and appraisal of performance”, Organizational Behavior and Human Decision Processes, Vol. 93, p. 47-61.

- Drogendijk, Rian; Slangen, Arjen (2006). “Hofstede, Schwartz, or managerial perceptions? The effects of different cultural distance measures on establishment mode choices by multinational enterprises”, International Business Review, Vol. 15, p. 361-380.

- Dodd, Olga; Frijns, Bart; Gilbert, Aaron (2015). “On the role of cultural distance in the decision to cross‐list”, European Financial Management, Vol. 21, p. 706-741.

- Erramilli, M. Krishna (1991). “The experience factor in foreign market entry behavior of service firms”, Journal of International Business Studies, Vol. 22, p. 479-501.

- Erramilli, M. Krishna; Agarwal, Sanjeev; Kim, Seong-Soo (1997). “Are firm-specific advantages location-specific too?”, Journal of International Business Studies, Vol. 28, p. 735-757.

- Erramilli, M. Krishna; Rao, C. P. (1993). “Service firms’ international entry mode choice: A modified transaction-cost analysis approach”, Journal of Marketing, Vol. 57, p. 19-38.

- Faccio, Mara; Masulis, Ronald W. (2005). “The choice of payment method in European mergers and acquisitions”, Journal of Finance, Vol. 60, p. 1345-1388.

- Faccio, Mara; McConnell, John J.; Stolin, David (2006). “Returns to acquirers of listed and unlisted targets”, Journal of Financial and Quantitative Analysis, Vol. 41, p. 197-220.

- Fishman, Michael J. (1989). “Preemptive bidding and the role of the medium of exchange in acquisitions”, Journal of Finance, Vol. 44, p. 41-57.

- Fuller, Kathleen; Netter, Jeffry; Stegemoller, Mike (2002). “What do returns to acquiring firms tell us? Evidence from firms that make many acquisitions”, Journal of Finance, Vol. 57, p. 1763-1793.

- Gaur, Ajai S.; Lu, Jane W. (2007). “Ownership strategies and survival of foreign subsidiaries: Impacts of institutional distance and experience”, Journal of Management, Vol. 33, p. 84-110.

- Ghosh, Aloke; Ruland, William (1998). “Managerial ownership, the method of payment for acquisitions, executive job retention”, Journal of Finance, Vol. 53, p. 785-798.

- Grinblatt, Mark; Keloharju, Matti (2001). “How distance, language, and culture influence stockholdings and trades”, Journal of Finance, Vol. 56, N° 3, p. 1053-1073.

- Han, Sam; Kang, Tony; Salter, Stephen; Yoo, Yong Keun (2010). “A cross-country study on the effects of national culture on earnings management”, Journal of International Business Studies, Vol. 41, p. 123-141.

- Hansen, Robert G. (1987). “A theory for the choice of exchange medium in mergers and acquisitions”, Journal of Business, Vol. 60, p. 75-95.

- Harrison, Graeme L.; McKinnon, Jill L.; Wu, Anne; Chow, Chee W. (2000). “Cultural influences on adaptation to fluid workgroups and teams”, Journal of International Business Studies, Vol. 31, p. 489-505.

- Harzing, Anne‐Wil (2002). “Acquisitions versus greenfield investments: International strategy and management of entry modes”, Strategic Management Journal, Vol. 23, p. 211-227.

- Hayton, James C.; George, Gerard; Zahra, Shaker A. (2002). “National culture and entrepreneurship: A review of behavioral research”, Entrepreneurship Theory and Practice, Vol. 26, p. 33-52.

- Hofstede, Geert (1980). Culture’s Consequences: International Differences in Work-Related Values. Beverly Hills, Sage Publications.

- Hofstede, Geert; Hofstede, Gert Jan; Minkov, Michael (2010). Cultures and Organizations: Software of the Mind. New York, McGraw-Hill.

- Hooghiemstra, Reggy; Hermes, Niels; Emanuels, Jim (2015). “National culture and internal control disclosures: A cross‐country analysis” Corporate Governance: An International Review, Vol. 23, p. 357-377.

- House, Robert J.; Hanges, Paul J.; Javidan, Mansour; Dorfman, Peter W.; Gupta, Vipin (2004). Culture, Leadership, and Organizations: The GLOBE Study of 62 Societies, SAGE Publications.

- Karampatsas, Nikolaos; Petmezas, Dimitris; Travlos, Nickolaos G. (2014). “Credit ratings and the choice of payment method in mergers and acquisitions”, Journal of Corporate Finance, Vol. 25, p. 474-493.

- Kim, W. Chan; Hwang, Peter (1992). “Global strategy and multinationals’ entry mode choice”, Journal of International Business Studies, p. 29-53.

- Kirkman, Bradley L.; Lowe, Kevin B.; Gibson, Cristina B. (2006). “A quarter century of culture’s consequences: A review of empirical research incorporating Hofstede’s cultural values framework” Journal of International Business Studies, Vol. 37, p. 285-320.

- Kluckhohn, Clyde (1962). “Universal categories of culture”, in Sol Tax (Ed.), Anthropology Today: Selections. Chicago, University of Chicago Press, p. 304-20.

- Kogut, Bruce; Singh, Harbir (1988). “The effect of national culture on the choice of entry mode”, Journal of International Business Studies, p. 411-432.

- Kreiser, Patrick M.; Marino, Louis D.; Dickson, Pat; Weaver, K. Mark (2010). “Cultural influences on entrepreneurial orientation: The impact of national culture on risk taking and proactiveness in SMEs ”, Entrepreneurship Theory and Practice, Vol. 34, p. 959-983.

- Kwok, Chuck C.Y.; Tadesse, Solomon (2006). “National culture and financial systems”, Journal of International Business Studies, Vol. 37, p. 227-247.

- Li, Jiatao; Guisinger, Stephen (1991). “Comparative business failures of foreign-controlled firms in the United States”, Journal of International Business Studies, Vol. 22(2), p. 209-224.

- Licht, Amir N.; Goldschmidt, Chanan; Schwartz, Shalom H. (2007). “Culture rules: The foundations of the rule of law and other norms of governance”, Journal of Comparative Economics, Vol. 35, p. 659-688.

- Loree, David W.; Guisinger, Stephen E. (1995). “Policy and non-policy determinants of US equity foreign direct investment”, Journal of International Business Studies, Vol. 26, p. 281-299.

- Luo, Yadong; Park, Seung Ho (2001). “Strategic alignment and performance of market‐seeking MNCs in China”, Strategic Management Journal, Vol. 22, p. 141-155.

- Martin, Kenneth J. (1996). “The method of payment in corporate acquisitions, investment opportunities, and management ownership”, Journal of Finance, Vol. 51, p. 1227-1246.

- Michailova, Snejina; Hutchings, Kate (2006). “National cultural influences on knowledge sharing: A comparison of China and Russia”, Journal of Management Studies, Vol. 43, p. 383-405.

- Murphy, Austin; Kevin, Nathan (1989). “An analysis of merger financing”, Financial Review, Vol. 24, p. 551-566.

- Offermann, Lynn R.; Hellmann, Peta S. (1997). “Culture’s consequences for leadership behavior: National values in action”, Journal of Cross-Cultural Psychology, Vol. 28, p. 342-351.

- Padmanabhan, Prasad; Cho, Kang Rae (1996). “Ownership strategy for a foreign affiliate: An empirical investigation of Japanese firms”, MIR: Management International Review, Vol. 36, p. 45-65.

- Redor, Etienne (2007). Les Méthodes de Paiement dans les Opérations de Fusions-Acquisitions: Richesse des Actionnaires, Sociétés Non Cotées et Déterminants. Thèse de doctorat, Université Lille 2.

- Reus, Taco H.; Lamont, Bruce T. (2009). “The double-edged sword of cultural distance in international acquisitions”, Journal of International Business Studies, Vol. 40, p. 1298-1316.

- Reuter, Charles (2011). “A survey of culture and finance”, Finance, Vol. 32, p. 75-152.

- Richards, Malika; De Carolis, Donna Marie (2003). “Joint venture research and development activity: an analysis of the international biotechnology industry” Journal of International Management, Vol. 9, p. 33-49.

- Roth, Kendall; O’Donnell, Sharon (1996). “Foreign subsidiary compensation strategy: An agency theory perspective”, Academy of Management Journal, Vol. 39, p. 678-703.

- Schwartz, Shalom H. (1999). “A theory of cultural values and some implications for work” Applied Psychology, Vol. 48, p. 23-47.

- Shane, Scott (1993). “Cultural influences on national rates of innovation”, Journal of Business Venturing, Vol. 8, p. 59-73.

- Shane, Scott (1994). “The effect of national culture on the choice between licensing and direct foreign investment”, Strategic Management Journal, Vol. 15, p. 627-642.

- Stahl, Gunter K.; Voigt, Andreas (2008). “Do cultural differences matter in mergers and acquisitions? A tentative model and examination”, Organization Science, Vol. 19, p. 160-176.

- Steensma, H. Kevin; Marino, Louis; Weaver, K. Mark; Dickson, Pat H. (2000). “The influence of national culture on the formation of technology alliances by entrepreneurial firms”, Academy of Management Journal, Vol. 43, p. 951-973.

- Taylor, Mark Zachary; Wilson, Sean (2012). “Does culture still matter?: The effects of individualism on national innovation rates”, Journal of Business Venturing, Vol. 27, p. 234-247.

- Tosi, Henry L.; Greckhamer, Thomas (2004). “Culture and CEO compensation”, Organization Science, Vol. 15, p. 657-670.

- Tsui, Anne S.; Nifadkar, Sushil S.; Ou, Amy Yi (2007). “Cross-national, cross-cultural organizational behavior research: Advances, gaps, and recommendations”, Journal of Management, Vol. 33, p. 426-478.

- Van Everdingen, Yvonne M.; Waarts, Eric (2003). “The effect of national culture on the adoption of innovations”, Marketing Letters, Vol. 14, p. 217-232.

- Wade-Benzoni, Kimberly A.; Okumura, Tetsushi; Brett, Jeanne M.; Moore, Don A.; Tenbrunsel, Ann E.; Bazerman, Max H. (2002). “Cognitions and behavior in asymmetric social dilemmas: A comparison of two cultures”, Journal of Applied Psychology, Vol. 87, p. 87-95.

- Weber, Yaakov; Shenkar, Oded; Raveh, Adi (1996). “National and corporate cultural fit in mergers/acquisitions: An exploratory study”, Management Science, Vol. 42, p. 1215-1227.

Parties annexes

Notes biographiques

Pascal Nguyen est professeur de finance corporative et ancien doyen de la faculté et de la recherche à l’ESDES Business School. Il est actuellement professeur invité à l’Université Hitotsubashi. Il était précédemment affilié à NEOMA Business School, à l’Université Technologique de Sydney et à l’Université de New South Wales. Ses intérêts de recherche concernent la gouvernance et la responsabilité sociale des entreprises. Il publie régulièrement sur ces sujets dans différentes revues internationales.