Abstracts

Abstract

Using a Value-at-Risk (VaR) approach and a sample of 2082 stocks on the 2004-2015 period, we measure the impact of SR dimensions (measured by Vigeo ratings) on the risk level and the risk dynamic of stock returns and on their risk predictability. We conclude that good overall socially responsible (SR) ratings reduce the downside risk level of stock returns. We find also that high-rated companies in HR (Human Resources), ENV (Environment), BB (Business Behaviour), CIN (Community Involvement), and HRTS (Human Rights at Workplaces) dimensions better absorb volatility shocks.

Keywords:

- Social Ratings,

- GARCH,

- Predictability Risk,

- Times Series Models,

- Value-at-Risk (VaR)

Résumé

En utilisant une approche par la Value-at-Risk (VaR) et un échantillon de 2082 actions sur la période 2004-2015, nous mesurons l’impact des dimensions socialement responsables (mesurées par les ratings Vigeo) sur le niveau de risque et la dynamique des risques des rentabilités d’action, ainsi que leur prédictibilité du risque. Nous concluons que le rating global RSE réduit le risque downside de la rentabilité des titres. Nous trouvons également que les entreprises bien notées dans les dimensions HR (Ressources Humaines), ENV (Environnement), BB (Comportement sur les Marchés), CIN (Engagement Communautaire), and HRTS (Droits Humains au Travail) absorbent mieux les chocs de volatilité.

Mots-clés :

- Ratings sociaux,

- GARCH,

- prédictibilité du risque,

- Modèles Time Series,

- Value-at-Risk (Var)

Resumen

Usando un enfoque de Value-at-Risk (VaR) y una muestra de 2.082 acciones durante 2004-2015, medimos el impacto de las dimensiones socialmente responsables (medidas con Vigeo ratings) en el nivel de riesgo y la dinámica de los riesgos de la rentabilidad de la acción, así como su predictibilidad del riesgo. Concluimos que la calificación general de CSR reduce el riesgo « downside ». También pensamos que las compañías que están altamente calificadas en HR (Recursos Humanos), ENV (Ambiente), BB (Comportamiento en los Mercados), CIN (Compromiso con la Comunidad) y HRTS (Derechos Humanos en el Trabajo) absorben mejor las crisis de volatilidad.

Palabras clave:

- Clasificaciones sociales,

- GARCH,

- Previsibilidad del riesgo,

- Modelos Time Series,

- Value-at-Risk (Var)

Article body

Numerous studies investigate the relationship between socially responsible (SR) dimensions or practices and company risk at both the theoretical and empirical level. Theoretically, due to better balancing the interests of the various stakeholders (Mishra and Modi, 2013), greater reputation (Godfrey et al., 2005) and less information asymmetry (Lahrech, 2011), companies with higher SR practices should be less risky and more resilient in times of crisis. However, as the risk measures (total risk, systematic risk and idiosyncratic risk), methodologies (for instance, measures of the various dimensions of social responsibility) and samples are heterogeneous, extant empirical studies do not provide clear evidence of these claims. Nonetheless, such studies suggest a slightly negative relationship between SR scores or ratings and financial risk measured as total risk (Jo and Na, 2012; Kim, 2010), idiosyncratic risk (Boutin-Dufresne and Savaria, 2004; Mishra and Modi, 2013; Bouslah et al., 2013) and systematic risk (Jo and Na, 2012; Kim, 2010).

Due to regulatory constraints (Basel 2-3) and equity optimization in banks, portfolio and risk managers use specific risk measures (namely, Value-at-Risk and Conditional Value-at-Risk measuring downside risk) but the effect of SR dimensions on these measures has to date only been partially investigated (Benlemlih and Girerd-Potin, 2014). Moreover, the question of how SR dimensions can improve the predictability of these measures remains unanswered. More specifically, we wonder if risk managers can use past returns, some characteristics of the company (size, leverage and CSR performance) to predict the mean and volatility of stock returns (mean and volatility are the two central parameters used to compute the Value-at-Risk). We are searching for a model specification and an information set (including SR ratings) among the set of models believed to be capable to predict expected returns and volatility[1]. Contrary to most studies on the relationship between SR dimensions and company risk, empirical studies in financial risk management often use GARCH like time series models in order to tend to account for several stylized facts (volatility clustering and leverage effect). Technically, risk measures are often predicted using an econometric times series model in the GARCH family. These kinds of measures permit to investigate the effect of SR dimensions on the time series properties of stock return volatility, even if not dealt in the literature until now.

In the present paper, we not only investigate the relationship between social rating and market risk level but also the risk dynamics and the risk predictability to assert whether the social rating can be used as an additional indicator of risk. We measure market risk levels by Value-at-Risk (VaR) while the risk dynamics are given by the parameters of a GARCH model. We then measure market risk predictability by observing how well standard parametric VaR modelling predicts extreme returns. Predictability is of practical interest for risk managers because if SR ratings help to better predict stock returns volatility, they could be introduced as valuable risk factors in risk prediction models.

We conclude of our empirical study using Vigeo ratings that in terms of the estimated risk characteristics, good overall SR ratings reduce the downside risk level (measured by VaR) and soften the volatility movements. When we decompose the results by SR dimensions, we find that high-rated companies in HR (Human Resources), ENV (Environment), BB (Business Behaviour), CIN (Community Involvement), and HRTS (Human Rights at Workplaces) dimensions better absorb volatility shocks than low-rated companies in the same dimension. Unfortunately, concerning the risk predictability, we do not find that SR ratings help to improve the prediction quality of stock return risk (measured by VaR)[2].

These results have interesting theoretical and managerial implications. From a theoretical viewpoint, to the authors’ knowledge, this paper is one of the first to investigate the SR dimensions-risk relationship measured by VaR while also measuring the impact of these dimensions on the risk dynamics of stock returns and risk predictability using a large international sample and sophisticated econometric models. From a managerial viewpoint, this research provides portfolio managers with the possibility of considering good SR practices (by dimensions) to reduce the ‘risk-VaR’ of their portfolios and the effect of negative returns on volatility while improving their capacity to soften the volatility movements of their portfolios.

The remainder of the paper is structured as follows. We first provide the theoretical foundations of the relationship between SR practices and company risk and review the empirical evidence of this relationship (sections 2 and 3). We then introduce our method and sample (section 4), present our empirical results (section 5) and end with our conclusions.

Theoretical Foundations of SR Dimensions or Practices and Company Risk

Some arguments developed in literature explain the relationship between social performance and financial risk (for a review, see Benlemlih and Girerd-Potin, 2014 and Kim et al. 2014). The impact of SR commitment on company risk has generated a theoretical debate between stakeholder theory and the more traditional stockholder governance approach. The debate could be seen under two prisms: the impact of SR dimensions on downside risk (reduce or increase the potential loss or negative risk) and on upside risk (reduce or increase the potential gain or positive risk).

The impact of SR commitment on downside risk

The impact of SR commitment on the intangible capital and the company risk

A first dimension of the debate is the answer to the following question: Does SR commitment increase or decrease the intangible capital of the firm? Intangible capital has a strong link with company risk because as for the traditional equity capital, relational and reputation capital can be seen as a buffer protecting the company against risk. According to Fombrun et al. (2000), “reputational capital safeguards the existing assets of the firm, serving as a buffer against losses”.

Stakeholder theory (Freeman, 1984) suggests that managers should balance the interests of shareholders, employees, customers and the community to ensure the organization’s survival. Indeed, achieving the organization’s objectives may depend on the interests of different stakeholders. Good SR practices reduce the risk of losing the support of one or more stakeholders. This leads to avoiding punitive measures that could otherwise result in decisions that have a negative effect on stakeholder interests. By developing good environmental, product and commercial practices, workplace quality of life, investor trust and other intangible advantages, SR companies will thus benefit from the lesser likelihood of legal actions resulting in financial penalties, higher employee loyalty and stronger customer trust (Boutin-Dufresne and Savaria, 2004).

Moreover, by increasing social performance and meeting stakeholder expectations, companies preserve and develop their reputation. Reputation is an important intangible asset affecting firm value and producing potential tangible benefits (Godfrey et al., 2005). The impact of reputation on financial performance is mainly due to insulation from negative financial performance. Participating in some types of SR activities leads to a form of goodwill or moral capital (Godfrey et al., 2005) that protect many of the firm’s relationship-based intangible assets, providing shareholders with insurance-like protection and contributing to shareholder wealth.

However, following the classical governance theory, SR commitment has a negative effect on relational or intangible capital because adoption of SR strategies could exacerbate the agency problem between managers and shareholders or stakeholders (Friedman, 1970). This SR engagement could be seen as a way to enlarge managerial discretion without corresponding enlargement of control. Managerial discretion deteriorates into self-interested opportunism risky to investors (Windsor, 2006).

The impact of SR commitment on the company’s efficiency and risk

The second dimension of the debate is the impact of SR adoption on companies’ efficiency. Following the stakeholder theory, high quality relationships with stakeholders have a positive effect on risk management by reducing uncertainty in the market place, creating controls that minimize or eliminate disruption, loss or damage to business operations, and reduce the impact of an undesirable event on the business (Kytle and Ruggie, 2005). More specifically, SR practices adoption and compliance with environmental and social issues improve the firm’s ability to control and reduce environmental and other risks such as damage to brand image, reputation and trust, consumer boycotts, high exposures to fines, penalties and punitive damages.

In the corporate governance perspective, adoption of SR strategies can increase risk because it deteriorates the competitive advantage of the company by diverting resources towards less or non-profitable activities (MacWilliams and Siegel, 2001) or by degrading the quality of decisions due to multi-objectives function (Jensen, 2001).

The impact of SR commitment on information asymmetry and company risk

The third dimension of the debate is on the impact of SR commitment on information asymmetry. Less information asymmetry and high information quality in business decisions also have the effect to reduce the risk perceived by investors and more generally by stakeholders (Lahrech, 2011). SR adoption should lead company to be more transparent and to disclose more reliable information to stakeholders. Several empirical studies illustrate the positive impact of SR adoption on the quality of information disclosure (Choi and Pae, 2011; Martínez-Ferrero et al., 2015). Nevertheless, following the second explanation, adoption of SR strategies could help managers to hide bad information (Jin and Myers, 2006) and bad behaviour (Hemingway and Maclagan, 2004). More specifically, SR activities can be used by manager to manipulate earnings (Prior et al. 2008) or to disguise the real value of a company’s assets (Zahra et al., 2005). As stated by Kim et al. (2014: 2), “if firms use CSR as a tool to disguise bad news and divert shareholder scrutiny, CSR would be associated with higher, not lower, stock price crash risk.”.

The impact of SR commitment on upside risk

All the previous explanations emphasis on the impact of SR adoption on downside risk (does it increase or not the risk of losses) but SR adoption could also have an impact on upside risk (possibility to decrease or increase the potential gain).

As every innovative process, adoption of SR strategies could generate new business opportunities. For instance, the company embodies its products with SR attributes but if customers could not enjoy these new attributes and be willing to pay for them, this strategy decreases the upside potential (upside risk) of the company (MacWilliams and Siegel, 2001). All initiatives considered to be socially responsible will distance leaders from their purported goal of maximizing profit (Aupperle et al., 1985). Preston and O’Bannon (1997: 421) talk about “trade-off hypothesis”, where SR activities “may siphon off capital and other resources from the firm, putting it at a relative disadvantage compared to firms that are less socially active.”.

In the other side, SR commitment can also be a vector of growth in sales and profitability (increases upside risk). SR practices could be viewed as a real opportunity of growth for companies if we integrate that many investors or consumers are ethical-focused and mainly interested in the quest for an ethical value rather than a financial value (Arvidsson, 2009). For instance, all the different issues around climate change and the new regulations (Paris Agreement, Carbon Disclosure Project, Montreal Pledge…) could act as real business opportunities for companies in developing SR strategies. This argument is linked to the social impact theory of Preston and O’Bannon (1997), for whom external reputation and social expertise develop economic and financial performance in creating competitiveness and differentiation. All these arguments are online with the stakeholder theory of Freeman (1984) where the success of a company is materialized when good relationships are maintained and developed with stakeholders (either internal or external).

Finally, the link between the systematic and idiosyncratic risk can be made in explaining how SR commitments attract SR investors on the market who are willing to pay more for this. Beltratti (2003) explains that the effect of ethical or socially responsible investing on stock prices is weak until the share of SR investors is reduced. However, as stated by Dupré et al. (2009), when this share is growing, SR stocks prices increase, as SR investors are willing to pay more and make a financial sacrifice to satisfy their SR positioning and requirement. Possibilities to generate market positive returns for SR investors is thus existing. As a consequence and a positive event for companies, the equity cost decreases for companies that demonstrate SR commitments and procure them a competitive advantage compared to non-SR companies by a reducing their funding rate and thus a better control of their financial risk (idiosyncratic risk). The innovation proposed by SR companies offer them the possibility to benefit from the capital of new investors identified as socially responsible. The role of SR funds is to identify and invest into SR companies and offer them the possibility to fund their growth opportunities. The specific market of SR investing (SRI), favoured by regulation and transformation of business models of investors considering the sustainable issues, permits to link SR companies and SR investors and thus to amplify positive events specific to the firm[3].

Finally, our arguments in the specific paragraph on upside risk try to demonstrate that SR companies have the possibility (but it is not sure) to obtain high positive returns (new opportunities, businesses, innovation, differentiation)[4]. We suppose that, due to better relationship with all the stakeholders, better reputation and a more sustainable business, the SR companies will suffer less of negative shocks (either idiosyncratic such as scandals, business disruptions… or systematic, for instance an increase of oil prices) and benefit more of positive shocks (either idiosyncratic or systematic) by attracting more quickly and efficiently the resources that are necessary for their growth. Consequently, the payoffs of SR companies should be closer to call option like payoffs than other companies.

Empirical Evidence of SR Dimensions or Practices and Company Risk

This section presents a literature review of the impact of SR dimensions on various measures of risk: total risk, systematic risk (theoretically rewarded by the market) and idiosyncratic risk (theoretically not rewarded by the market[5]). We isolate the few studies on downside risk as these constitute the measures used in this paper.

Total, idiosyncratic and systematic risk

Some empirical studies examine the relationship between SR dimensions or practices and financial risk through components of total risk (measured by variance or standard deviation of stock returns), systematic risk (or market risk) or specific risk (or idiosyncratic risk).

Using a meta-analysis, Orlitzky and Benjamin (2001) reconsider various empirical studies addressing the link between social performance and financial risk in the US between 1978 and 1995. Their results support the existence of a negative relationship between these two variables. More recently, Jo and Na (2012) and Kim (2010) studied the relationship between SR practices of companies and firm total risk using respectively KLD data and The Business Ethics 100 Best Corporate Citizens in the American market. Jo and Na (2012) conclude that firm total risk is negatively related to SR engagement. The reasons why empirical literature yields few significant relations between SRI and expected returns are noted and may be due to the aggregation of different dimensions that have contrasting effects (Scholtens and Zhou, 2008). This therefore requires investigating different dimensions of social responsibility. Kim’s (2010: 205) results illustrate this point: “composite CSR” measures show a positive effect while some individual “components of CSR” measured with the business ethics score show a negative effect on total firm risk.

In terms of idiosyncratic risk, the results of empirical studies do not provide clear evidence on the negative effect of SR dimensions or practices. Most studies find a negative relationship with firm idiosyncratic risk (Boutin-Dufresne and Savaria, 2004; Mishra and Modi, 2013), yet Humphrey et al. (2012) and Kim (2010) find no evidence. Finally, Bouslah et al. (2013) focus on individual components of social performance and find that idiosyncratic risk is negatively related to employee relations and human rights, while other SR components do not affect financial risk. This study supports the notion that not all SR dimensions are relevant in evaluating a company’s risk.

SR engagement also has an effect on systematic risk. Studies on the US markets (Jo and Na, 2012; Kim, 2010) find that corporate social performance is negatively related to systematic risk. However, Oikonomou et al. (2012) show that individual KLD[6] strength components are negatively but insignificantly related to systematic risk while three out of five individual social concerns (community, employment and environment) have a positive and significant effect. Salama et al. (2011), focusing on environmental responsibility using a sample of UK firms, find that the environmental performance of these firms is inversely related to systematic risk.

From a general viewpoint, extant literature suggests there is a slight negative relationship between SR dimensions or ratings of companies and the different measures of financial risk (stock volatility, idiosyncratic risk and systematic risk).

Downside risk

Few studies analyse the impact of SR ratings on downside risk measures. Nofsinger and Varma (2014) show that SRI funds perform better during bear markets as their attributes dampen downside risk. Oikonomou et al. (2012) show no significant effect of KLD ratings on financial risk when using the Bawa and Lindenberg beta downside risk measure, while their Harlow and Rao beta results analysis shows a positive relationship between downside risk and some individual components of social irresponsibility (community concerns, employee relation concerns and environmental performance concerns). Benlemlih and Girerd-Potin (2014) use ‘Value-at-Risk’ (VaR) and ‘Conditional VaR’ (CVaR) measures of downside risk and find that portfolios with high social responsibility scores are less risky than portfolios with low social responsibility scores. Finally, the study of Kim et al. (2014) supports the mitigating effect of CSR on crash risk defined as the conditional skewness of return distribution.

Methodology and sample

Value-At-Risk Methodology

We use the Value-at-Risk framework to assess stock market risk. In recent years, the tremendous growth in trading activity and the widely publicized trading losses of well-known financial institutions have led financial regulators and supervisory authorities to favour quantitative techniques that appraise the possible losses that these institutions may incur. Value-at-Risk has become one of the most widely used techniques as it provides a simple answer to the following question: with a given probability (say α), what is my predicted financial loss over a given time horizon? The answer is the VaR at level α, which gives an amount in the currency of the traded assets (in dollar terms for example) and is thus easily understandable. VaR has a simple statistical definition: the VaR at level α for a sample of returns is defined as the corresponding empirical quantile at %. The quantile definition implies that with probability 1 -α the returns will be larger than the VaR. In other words, with probability 1 -α, the losses will be smaller than the dollar amount given by the VaR. From an empirical point of view, computing the VaR for a collection of returns thus requires computing the empirical quantile at level α of the distribution of the returns of the portfolio.

Formally, the conditional VaR (for a long position) can be defined as:

Modelling the stock returns process

The necessary elements to compute VaR are the volatility and mean of the returns process. We consider a collection of daily log returns (in %), yt = 100[log (pt ) − log (pt−1)] where t = 1,…T and pt is the stock price at time t. We rely on the ARMA-GARCH and the ARMA-GJR model to forecast the mean and variance process, The ‘ARMA’ part forecasts the conditional mean process (μ) while the ‘GJR’ part forecasts the conditional variance process (σt). The ARMA orders (p,q) are determined by minimizing the Akaike information criterion with p,q=0: 1 (four combinations). Accordingly, the conditional mean process equation is:

To model the conditional variance process, we use the classical GARCH and the GJR Models (which allows modelling asymmetric volatility clustering). The conditional variance process is defined as:

where S–t−1 is a dummy variable that takes the value 1 when εt is negative and 0 otherwise. This term (specific to the GJR model) permits the effect of a shock ε2t on the conditional variance σ2t to differ when the shock on returns is positive or negative. This asymmetric effect in financial series is widely documented: volatility increases by a greater amount following negative shocks and is often associated with the ‘leverage effect’ whereby a firm’s debt-to-equity ratio increases when equity values decline, and equity holders perceive the firm’s future income streams as more risky (Black, 1976). The GARCH model is a restricted version of the GJR model, with γ = 0. We set the order of lag to be (1,1) for all variance models.

In the present paper, we adopt an out-of-sample methodology to compute VaR, which entails an iterative procedure where forecasts are made as in ‘real’ conditions, meaning that the estimation part that calibrates the model does not include observations of the forecast period but is updated daily in the same way practitioners do. The estimation part is based on a minimum of five years of data regularly updated with the most recent days. This out-of-sample methodology is coupled with an update of the econometrical model every 50 trading days. Calibrated (to the data) models are used to predict one-day ahead the future mean and variance process allowing the authors to compute ex-ante the one-day ahead VaR (long and short positions).

The procedure can be summarized as follow:

Starting with an initial sample of five years of data, for each series we calibrate the model and predict the following day’s (t+1) conditional mean (

) and variance process ().

) and variance process ().Moving to one day ahead, we observe the realized values (σ2t, yt) and compare this with the predicted values (

, ) and store the result. We then add this day in the estimation sample and predict the following day’s mean and variance values. We repeat the second step until we reach the end of the sample and update the model calibration (parameters are estimated via maximum likelihood estimation) every 50 days.

We observe the number of violations[7] for both the long and short positions and deduct the theoretical annual VaR based on the conditional mean and variance process. We then derive statistical significance for the quality of the VaR estimation. These results and the VaR parameters are stored annually per stock and used later on in the panel data analysis.

In addition to the standard long VaR computation, we also consider the short VaR as in Giot and Laurent (2003). The long side of the daily VaR is defined as the VaR level for traders with long positions in the relevant stocks, which is the ‘usual’ VaR where traders incur losses when negative returns are observed. Correspondingly, the short side of the daily VaR is the VaR level for traders with short positions, i.e., traders incurring losses when stock prices increase. The model’s ability to predict long VaR thus relates to its ability to model large negative returns, while its performance regarding the short side of VaR is based on its ability to take into account large positive returns.

For the normal GARCH model, the VaR for long and short positions is given by:

where Nα (N1-α σt) is s the left (right) quantile at α% for the normal and ut and σt are respectively the conditional mean and conditional variance at time t. We set α to the value 0.05.

Evaluation of the quality of the VaR estimation

Our aim is to evaluate to which extent the VaR methodology accurately predicts extreme returns and whether this accuracy is linked to social ratings. We thus focus on so-called ‘VaR violations’. The expected number of violations depends on the confidence level, Let It (α) denote the exception variable associated with the ex-post observation of an α% VaR exception at time t for a long position case, It (α) is then defined as:

VaR forecasts are valid if and only if the violation process satisfies the Unconditional Coverage Property and the Independence Property (Christoffersen, 1998). We rely on the most distinguished Dynamic Quantile Test of Engle and Manganelli (2004) to jointly test whether these two conditions are satisfied, i.e., that the frequency of exceptions is consistent with the expected number of violations (Unconditional Coverage Property) and that violations are independently distributed (Independence Property).

The Dynamic Quantile is based on a simple linear regression that links the violations to the lagged violations. Violations are represented by the Hit variable defined as follows (for long position VaR):

The Hit variable takes values 1 − α every time rt < −VaR and − α otherwise. The intuition is as follow: if the intercept of the regression is null, it indicates that the Unconditional Coverage Property is fulfilled (E(Hitt) = 0), additionally if all the coefficients (of the lagged Hits) are also null this show that there is no correlation in the Hit sequences and then that the Independence property is also fulfilled. Engle and Manganelli (2004) show that, under the null hypothesis of adequate modelling, the Dynamic Quantile Statistic (see equation below) follows a Chi-Square distribution. The test statistic is given by:

where β is a vector composed of the regression coefficients on the lagged hits, X is the explanatory variable matrix (lagged hits) and k depends of the number of explanatory variables (number of lags). In our case, we include 5 lagged Hit variables (for technical details, see Dumitrescu et al., 2012) so the matrix X corresponds to a matrix composed of 5 times-series of daily violations (dummies vector with value 1 if one hit and 0 otherwise) based on the original Hit sequence but at 5 different lags. In the following, we present our two econometric panel data models.

Sample

We use Vigeo social ratings[8] to measure the link between SR dimensions and financial risk. In other words, we want to test the influence of the social ratings of companies on their level of risk. We consider Vigeo SR dimensions given that it is the leading European agency and that it considers worldwide firms. The vast majority of empirical studies have used KLD (MSCI ESG Research today gathering KLD, Innovest and IRRC) ratings or databases to measure the link between SR ratings and financial performance or risk. The advantage to use Vigeo ratings is to provide new information on this relationship in using data extracted and collected with another methodology and others dimensions of SR, with an objective to provide new conclusions and new issues in a worldwide context when KLD database provides only American data. Moreover, recent studies use Vigeo database (Girerd-Potin et al., 2014; Liang and Renneboog, 2016; Quéré et al., 2018).

Vigeo rates companies on six dimensions: ‘Environment’, ‘Corporate Governance’, ‘Human Rights at workplaces’, ‘Human Resources’, ‘Business Behaviour’ and ‘Community Involvement’[9]. It differs from KLD dimensions based on seven themes: ‘Community Relations’, ‘Corporate Governance’, ‘Diversity’, Employee Relations’, Environment’, ‘Product’ and ‘Human Rights’ (rated on strengths and concerns for each dimension when the rating provided by Vigeo is for a date, for a sector and for each dimension and sub-dimension). As the methodology of KLD and Vigeo totally differ, ratings will automatically be different.

To rate a company, Vigeo uses two types of scales: ‘Vigeo scores’ and ‘Vigeo ratings’. Vigeo scores consist to attribute a score to a company between 0 for the least socially responsible firms to 100 for the most responsible firms (the score provided is not relative to the sector). Vigeo ratings consists to provide a score to a company relative to its sector on five levels: --; -; =; + or ++. We decide to use ‘Vigeo ratings’ in our study to be sure that companies are rated relative to their sector.

Each rate is given a numerical value from 1 to 5, where 1 and 5 are respectively the extreme rates “--” and “++”. Thus, Vigeo ratings are treated as categorical variables.

The daily returns obtained from Datastream from 1 January 2000 until 31 December 2015 for all common shares with a Vigeo social rating resulted in a sample of 3523 companies all of size and sectors. The following filters were then applied:

Datastream stocks with available prices

Less than 10% missing data for each stock per year

Stock with at least five consecutive years of data (a requirement for Value-at-Risk estimates).

The final sample consisted of 2185 eligible companies rated by Vigeo and from which we can estimate the parameters of the time series models of stock returns. But considering that for some companies we have no possibility to match the data (for instance, for a given company, we can estimate the parameters of the time series models for 2007-2008 but obtain the SR rating only for 2009), our final sample is thus composed of 2082 eligible companies.

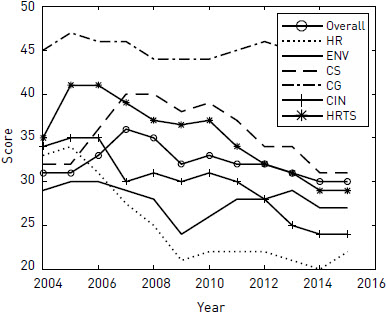

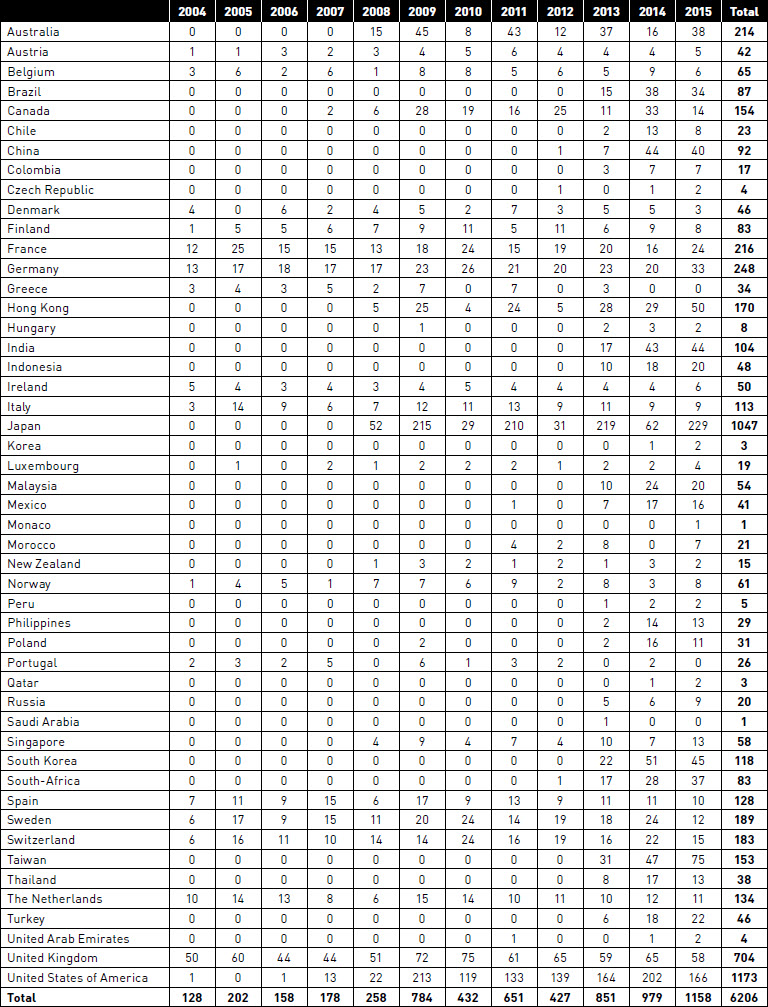

Table 1a provides the summary statistics for each of the original ratings, size (measured by the Log of market value) and leverage. We observe that mean and median values are close. The global score is around 31 (mean 31.84; median 31). Companies obtain the lowest score on the Human Resources dimension (mean 24.64; median 22) and the highest score on the dimension under intensive scrutiny of the investors i.e. Corporate Governance (mean 41,53 median 43). From table 1b we observed that USA, Japan and UK represent respectively 18.9%, 16.87% and 11.34% of the total sample followed by Germany, France, Australia with about 3% each. Europe represents majority of data considering that Vigeo is a European company. Note also that the number of ratings is increasing until 2009 (during the financial crisis) then decreases until 2012 and finally increases again. Half of the ratings are measured from 2013 to 2015. Finally, we observe from figure 1 that the median scores of SR dimensions are globally decreasing over time (between 2004 and 2016), certainly due to the increasing number of rated companies through time and thus the heterogeneous SR commitments of companies between emerging and experienced markets on sustainable issues.

Impact of SR dimensions on market risk characteristics

Since the computation part is performed daily for individuals stocks while storing the results at the annual frequency, we obtain cross-sectional time series data. To unveil the relationship between market risk and SR rating, we employ an (unbalanced) panel data model. To distinguish also the use of empirical and theoretical VaR, we precise that we use the empirical VaR as a (raw) proxy to assess the market risk and the theoretical VaR as a proxy (DQT Test) to assess the market risk predictability.

The static single equation model is given by:

where riski,t is the dependent variable to determine (market risk) with i denoting individuals and t denoting time, ηi and δt are respectively individual effects and time specific effects. riski,t represents risk measure or characteristics as described below, Xi,t is an independent variable vector corresponding to the rating of one the 6 SR dimensions (HR, ENV, BB, CG, CIN, HRTS) or the overall rating, 2 variables corresponding to firm’s characteristics (MV, Leverage), and a constant. β is an unknown coefficient associated to a SR dimension, ηi is a random variable possibly correlated with X'i,t (Fixed Effect) but uncorrelated with the error term vi,t.

MV and Leverage are, respectively, the market capitalization and leverage ratio (Total Debt /Capital). We include the leverage ratio to disentangle the financial leverage risk (captured per the leverage ratio) from the business risk. Market capitalization is introduced to control the fact that small-caps stocks are riskier investments than large-cap stocks.

We estimate fixed effect model because we suspect omitted variables to be correlated with the explanatory variables (it is likely the case with the capitalization variable) and because observations can hardly be considered as being a random sample from the full population (over-representation of the USA). Moreover, the Hausman (provided in Appendix 2) confirm the superiority of the Fix estimator vs the Random Estimator.

We consider the following dependent variables to evaluate the relationship between SR dimensions and market risk:

The empirical Value-at-Risk values computed as the 5% quantile of returns on a yearly basis.

The three parameters of the conditional variance: the asymmetric parameter of the GJR Model (the so-called ‘leverage effect’ parameter) and ARCH and GARCH parameters (respectively γiGJR αiGJR and βiGJR of equation (3)).

The average (daily) returns. This variable is included to test for a potential effect of SR dimensions on rentability.

The average daily variance as an additional proxy for risk (total risk).

To summarize, the equations model is formally stated as:

where Yeart is a year dummy variable, β1 is the coefficient of the Vigeo rate and β2 and β3 are control variable coefficients. The dependent variable Y (riskit,) successively takes the following five variables: the empirical Value at Risk for 1) Long and 2) Short position, 3) the Leverage coefficient βiGJR, 4) the ARCH βiGJR coefficient and 5) the GARCH parameters βiGJR of the conditional variance process. We also estimate the model by replacing the SR dimension by the overall rating as an explanatory variable. This continuous variable differs of the other ratings variables that are categorical variables. The overall rating is computed as a weighted average of the six SR dimensions and expressed with respect to the firm’s sector (the formula is not publicly disclosed by VIGEO).

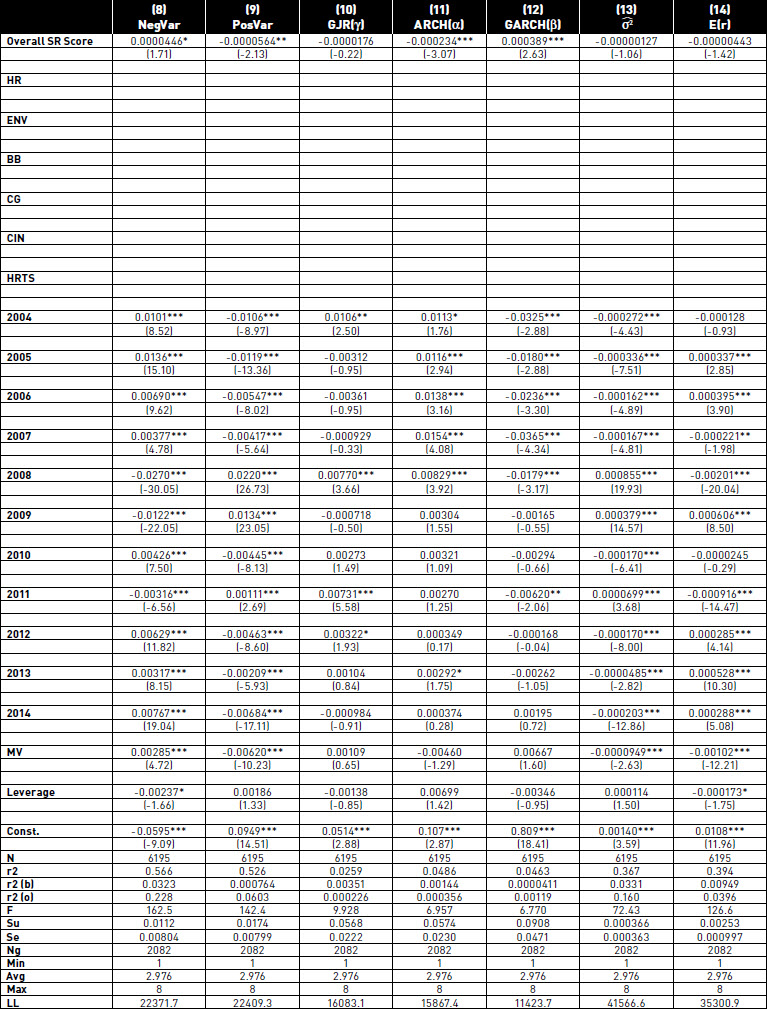

Table 1a

Summary statistics of Vigeo’s SR scores

This table summarizes the six Vigeo scores (Environment (ENV), Corporate Governance (CG), Human Rights at workplaces (HRTS), Human Resources (HR), Business Behaviour (BB) and Community Involvement (CIN). MV and Leverage refer respectively to the ‘log of market capitalization’ and the ‘ratio of debt over total assets’.

FIGURE 1

Evolution of median Vigeo SR scores for each SR dimension

Table 1b

Summary statistics: distribution of the sample by years and countries

If SR commitment reduces risk, we should expect the following impacts:

ARCH effect: the impact of SR ratings on αi of formula (3) should be negative, recent chocks have a lesser effect on future risk (better capacity of SR companies to absorb chocks),

GARCH effect: the impact of SR ratings on βi of formula (3) should be positive, the variance process is more stable in time, risk should be easier to predict.

Asymmetric effect: the impact of SR ratings on yi of formula (3) should be negative. Indeed, a positive coefficient would mean that impact of negative chocks on volatility increases with good SR ratings. However, we expect the opposite because good SR ratings may be perceived by equity holders as a positive signal about the firm’s future risk.

Impact of SR dimensions on market risk predictability

As previously stated, we use the DQT test to assess VaR accuracy as a proxy of market risk predictability. We therefore observe two scenarios: 1) either the DQT test accepts the null hypothesis of adequate VaR prediction, or 2) the VaR prediction fails and the model does not capture the return dynamics. We classify as successful whenever the null hypothesis of the DQT test of adequate modelling is accepted at a 5% confidence level. Thus, for each firm and each year, we obtain a time-series of a binary variable indicating success or failure regarding the VaR prediction.

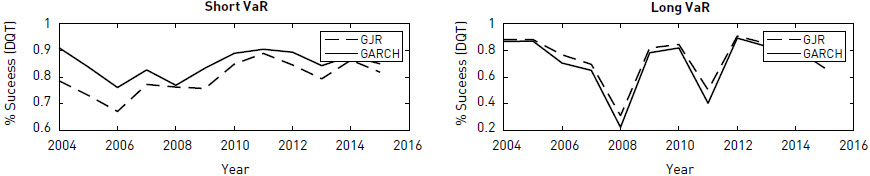

Figure 2 presents a comparison of the ARMA-GARCH and ARMA-GJR models using the DQ test. The classical GARCH obtains better results for the risk (VaR) of short positions and GJR for the risk of long positions. In the empirical analyses, we will therefore use the classical GARCH model when the dependant variable is the “short VaR” and the GJR model when the dependent variable is the “long VaR”. Note that the percentage of success is quite low during crisis periods (2008 and 2011, crisis in the euro-zone) meaning that prediction quality of time series models deteriorate in period of crisis when risk predictability is more needed.

FIGURE 2

Comparison of the GARCH and GJR time series models in the case of long and short portfolios

To evaluate the relationship between SR dimensions and this VaR accuracy, we use a fixed-effects logistic regression. The dependent variable (RQP, risk quality prediction) can take only two states: 0 for failure in predicting VaR or 1 for success in predicting VaR. The logistic model is therefore suitable. The dependent variable is derived of the DQT obtained via the ARMA-GARCH to evaluate short position and via the ARMA-GJR to evaluate long position.

Formally the fixed-effects logit model is[10],

Xi,t is a vector of observations on the explanatory variables (SR dimensions and overall rating) and is a vector of unknown coefficients. The same explanatory variables as in the non-logit panel case are included. Estimation is implemented using Matlab and Ox programming language (Doornik, 2007) with G@rch (Laurent and Peters, 2002).

Empirical Results

SR ratings and market risk characteristics

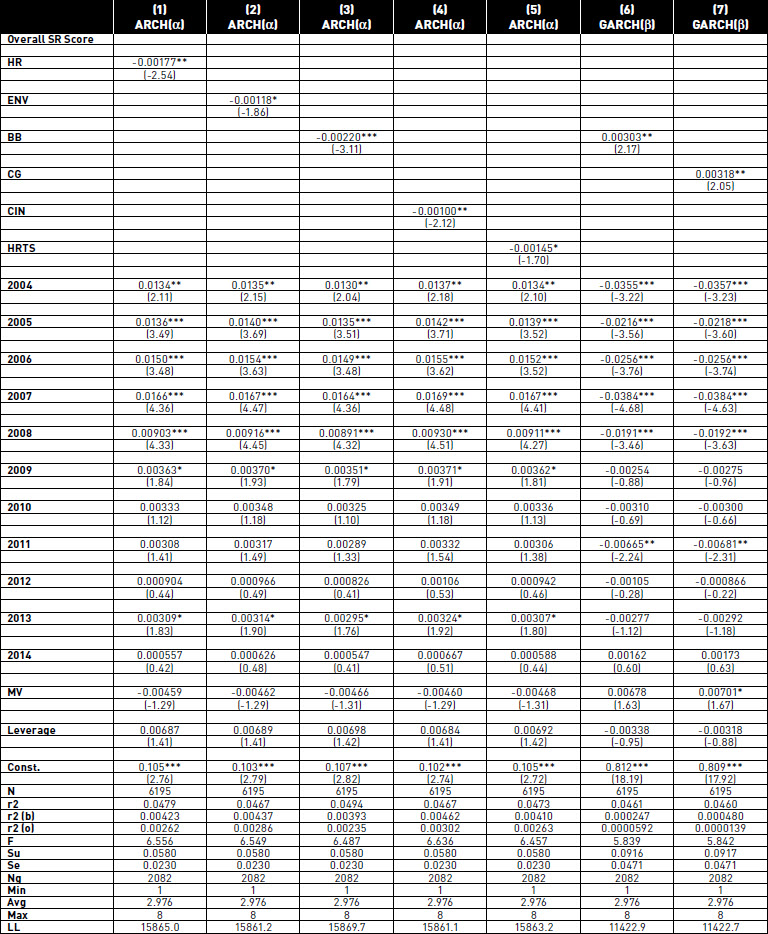

Table 2 presents the results of the effect of the SR ratings on the VaR of long and short positions and on the parameters of the GJR GARCH model. We only report regressions that have a significant SR coefficients.

Empirical value at risk - market risk

In terms of the Empirical Value at Risk (column (8) and (9) of table 2), the size (Market Capitalization) tends to reduce market risk since it lowers positive VaR (significantly) and increases negative VaR. Conversely, and as expected, the debt ratio (Leverage) increases market risk since it is positively related to extreme variation (increasing positive VaR and lowering negative VaR). SR involvement (measured by the overall SR rating) tends to reduce risk because coefficient is significantly positive for negative VaR and negative significant for positive VaR. We do not find significant impact of SR dimensions on positive or negative VaR. SR commitment seems to have a synergetic effect: it is only when the company is engaged in a global SR implementation (and not particularly specific for dimensions) that the impact on risk reduction is significant.

Table 2

SR scores and market risk characteristics: Fixed effect panel data model

Table 2 (continuation)

* p < 0.10, ** p < 0.05, *** p < 0.01.

r2, r2(b) and r2(o) denote, respectively, the within, between and overall r-squared. F is Fischer statistic and Su and Se are respectively the panel-level standard deviation and standard deviation of vit. N, Ng, Min, Avg and Max refer, respectively, to the total number of observations, the total number of groups, the minimum, average and maximum number of groups. The dependent variables N-VaR, P-VaR, GJR, ARCH, GARCH, ( ) and E(r) refer respectively to the negative empirical VaR, positive Empirical VaR, the asymmetry parameter of the GJR model, the ARCH coefficient, the GARCH coefficient, the (daily) variance and the (daily) average returns. T-statistics are given in parentheses. LL is the log-likelihood. Standard errors are cluster–robust standard errors.

) and E(r) refer respectively to the negative empirical VaR, positive Empirical VaR, the asymmetry parameter of the GJR model, the ARCH coefficient, the GARCH coefficient, the (daily) variance and the (daily) average returns. T-statistics are given in parentheses. LL is the log-likelihood. Standard errors are cluster–robust standard errors.

As stated above, good global SR rating (overall rating) reduces significantly the VaR of short and long portfolios. Nevertheless, the impact of good global SR rating on variance is also negative but not significant (table 2, column 13). These results tend to show that SR strategy is more efficient in reducing extreme risks (kurtosis) than global risk (variance). Furthermore the impact of global rating on expected returns is negative (meaning, following equations (4) and (5), that it increases the long position risk and decreases the short position risk) but non-significant. In consequence, our VaRs do not suffer of a potential mean effect (table 2, column 14).

Asymmetric parameter[11]

Regarding the asymmetric parameter of the GJR Model, we observe a non-significant relation between the overall SR rating and the asymmetry coefficient (column (10) in table 2). This finding indicates that SR involvement has no perceivable impact on the leverage effect. Leverage has the same effect on stock prices behaviour for high and low SR companies. This result has a practical consequence because it means that high SR companies cannot increase their leverage expecting a dampening effect of CSR on the asymmetric effect.

GARCH parameters

Finally, regarding the conditional variance process, we observe that BB (Business Behaviour) and CG (Corporate Governance) dimensions have a positive (significant) effect on the GARCH parameters, indicating higher persistence in the variance (column (6) and (7) in table 2)[12]. The coefficient is also positive and significant for the overall SR rating (column (12) in table 2). Volatility is therefore more stable for companies with higher SR ratings. Correspondingly, we observe negative significant coefficients for HR (Human Resources), ENV (Environment), BB (Business Behaviour), CIN (Community Involvement), and HRTS (Human Rights at Workplaces) dimensions (column (1) to (5) in table 2) for the ARCH effect. These results indicate that highly ranked companies in terms of each of these SR dimensions have a variance process that is less affected by shocks than low ranked companies. The overall SR rating has also a negative significant impact on the ARCH effect (column (11) in table 2) confirming that companies with high SR ratings are less sensitive to shocks.

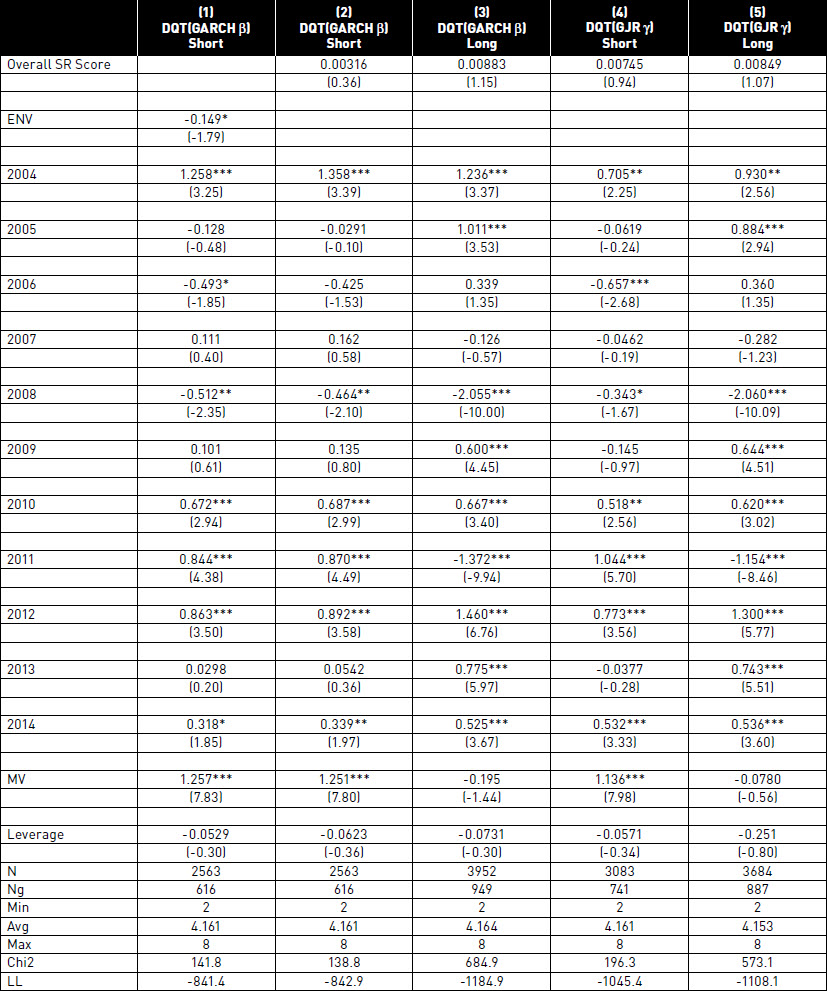

SR ratings and market risk predictability

The fixed-effects logistic regression results corresponding to equation (11) are reported in table 3 for the VaR of long and short positions using respectively the GJR and classical GARCH.

Firm size (measured by Market Capitalization) has a significant (at 1%) impact on the probability that the VaR methodology adequately predicts extreme variations for ‘short’ positions. This indicates that the probability of a correct VaR prediction for a large company is greater than for a small one. The positive and significant effect of the market capitalization variables also indicates that VaR prediction accuracy increases with firm size. Concerning Global SR ratings, we observe that its impact on risk prediction quality is positive but not significant (columns (2) to (5) in table 3). We report only one significant result in the table 3 for the SR dimensions: ENV (Environment) has a negative impact on the prediction of the short VaR (column (1) of table 3). During the crisis period the market risk predictability deteriorated as indicated by the negative and strongly significant coefficients of the year 2008.

Discussion and Conclusion

This paper examines the relationship between SR dimensions or practices and financial risk (measured by VaR) in an international context. The originality of this paper is in simultaneously proposing a measure of risk (Value-at-Risk) with a measure of the impact of SR Vigeo dimensions on the risk dynamics of stock returns and risk predictability.

While extant ‘CSR-Risk’ related literature focuses on the measure of this relationship, it has thus far been silent on the effect of SR dimensions on risk predictability and risk dynamics. Indeed, although knowledge on the relation between risk level and SR dimensions is certainly valuable, risk managers tend to take this risk into account with tools such as VaR models. Therefore, in addition to measuring the level of risk, evaluating the relation between SR dimensions and risk model characteristics and accuracy would also seem relevant.

As a main contribution, we find that high-rated companies considering SR global rating (defined as ‘Overall SR Rating’) appear to be less risky (in terms of downside risk level measured by VaR) than low-rated companies, dampen the effect of negative returns on volatility and soften volatility movements. This reinforces the argument that SR considerations allow more accurately anticipating and managing the social risk of a company and thus the financial risk through what Kurtz (2002) termed the ‘information effect’ (better control of environmental and social risks lead to better anticipating financial risk).

When we decompose the results by SR dimensions for the estimated risk characteristics, we find that high-rated companies in HR (Human Resources), ENV (Environment), BB (Business Behaviour), CIN (Community Involvement), and HRTS (Human Rights at Workplaces) dimensions better absorb volatility shocks than low-rated companies in the same dimension. Our results are therefore in line with the results of Bouslah et al. (2013) on the systematic risk of companies and reinforced by Boutin-Dufresne and Savaria (2004: 60) for HRTS, CIN, HR and BB dimensions. For the human rights issues (HRTS), the authors state that “the risks associated with the quality of life in the workplace at local and international levels are the loss of profitability resulting from, e.g., strikes, legal actions related to work safety, or sweat shop issues”. Concerning the community, social and commercial issues (CIN, HR and BB), we are online with the fact that “by its involvement in local communities through charity, for instance, the firm develops a better understanding of its market while the same forging a sustainable relationship with its stakeholders, thus possibly avoiding a commercial boycott in the future” (Boutin-Dufresne and Savaria, 2004: 60). The authors add that the more the firm is engaged in its daily activities into ethical and social issues, whether internal (employees for instance) or external (community), the lower the chances that the company will face legal actions or large-scale boycotts in the future. For the environmental issues (ENV), our findings confirm that enhancing environmental performance improves the productivity of the firm and its competitiveness in the long term as supported by Porter hypothesis (1991), and so on its financial risk.

Table 3

SR scores and market risk predictability: Conditional fixed-effects logit model

* p < 0.10, ** p < 0.05, *** p < 0.01.

N, Ng , Min, Avg and Max refer, respectively, to the total number of observations, the total number of groups, the minimum, average and maximum number of groups. A large number of groups has been dropped because some groups have the same dependent variable (vector with only one or zero values) whereas the estimation required at least two different outcomes. Chi2 and LL are respectively the statistic of the chi2 test and the log-likelihood of the model. t statistics are given in parentheses. The dependent variables DQT(GARCH) SHORT and DQT(GJR) LONG are binaries variable that indicate success (1) or failure (0) of the null of adequate VaR modelling based on the DQT test using results of the GARCH models for short position VaR and of the GJR model for the long position VaR (found to be the most appropriate model for each position).

Finally, concerning the risk predictability, we find only one negative significant relationship between the ‘Environment’ dimension and the statistical quality of the prediction of stock return risk (measured by VaR) for short sales. In consequence, it appears that from a practical point of view of risk manager, SR dimensions could not help them to better predict risk of stocks return using GARCH like time series models.

The theoretical and managerial implications of this research are multiple. From a theoretical viewpoint, our study confirms the results observed between SR dimensions and total, specific and idiosyncratic risks, starting to bridge the gap in the sphere of ‘CSR-downside risk’ using the VaR approach. Our methodology based on the study of risk dynamics and predictability enables going beyond the single ‘CSR-risk’ measure to understand how SR dimensions can absorb volatility shocks or dampen the impact of negative returns while considering the quality of the VaR prediction. Moreover, we consider that our results confirm that SR strategies could act as a way to include stakeholders utilities in the corporate objective function (to reduce risk in our perspective) and to integrate that they are not only under constraint of shareholder’s utility function as stated by Jensen (2001). From a managerial perspective, companies are encouraged to adopt SR strategies that could finally positively act on their risk management processes, as they could be a source of interest for portfolio managers and investors.

However, in terms of robustness, this study requires further evidence. Indeed, the question about the influence of SR commitment on company risk remains central and decisive to answer issues about profitability or performance. As MacGuire et al. (1988: 868) state: “… rather than looking for increased profitability from socially responsible actions, managers and those interested in the financial impact of social responsibility might look toward reduced risk. Since high risk must be balanced by high returns, firms with low social responsibility should earn high returns to justify the increased risk”.

Better risk management always entails more profitability in the long term, yet the inverse is not always true. The lack of conclusions in this sphere and especially in risk management through downside risk requires future research to encourage and nourish this debate, testing other data, markets and periods, to provide practitioners the ability to consider SR practices in their risk management processes.

Appendices

Appendices

Appendix 1. Vigeo Social Ratings

The Vigeo frame of reference has 38 generic criteria divided into 6 distinct domains:

Human Resources: constant improvement of professional and labour relations as well as working conditions.

Environment: protection, safeguarding, prevention of attacks on the environment, implementation of an adequate managerial strategy, ecodesign, protection of biodiversity and reasonable control of environmental impacts on the overall lifecycle of products and services.

Corporate Governance: efficiency and integrity, insuring the independence and effectiveness of the Board of Directors, effectiveness and efficiency of audit and control systems and particularly social responsibility risks, respect of shareholder rights and especially minorities, transparency and moderation in executive remuneration.

Community Involvement: effectiveness, managerial integration of commitment, contribution to economic and social development of the territories of establishment and their human communities, concrete commitment in favour of controlling the societal effects of products and services, transparent and participative contribution to causes of general interest.

Business Behaviour: taking into account clients’ rights and interests, integrating social and environmental standards both in the selection of suppliers and in the overall supplying chain, efficient prevention of corruption and respect of competition laws.

Human Rights at Workplaces: respect of trade union freedom and promoting collective negotiation, non-discrimination and equality, eradication of banned working practices (child and forced labour), preventing inhumane or humiliating treatments such as sexual harassment, protecting private life and personal data.

More precise definitions of these criteria are available on the Vigeo website: http://www.vigeo-eiris.com/fr/.

Appendix 2. Vigeo Social Ratings

This table displays results of the Hausman test applied on the regression presented in table 2. The Hausman test has for null hypothesis that the random effect model should be preferred, p-values are below 0.01 indicating that the alternative, the fixed effect model should be employed.

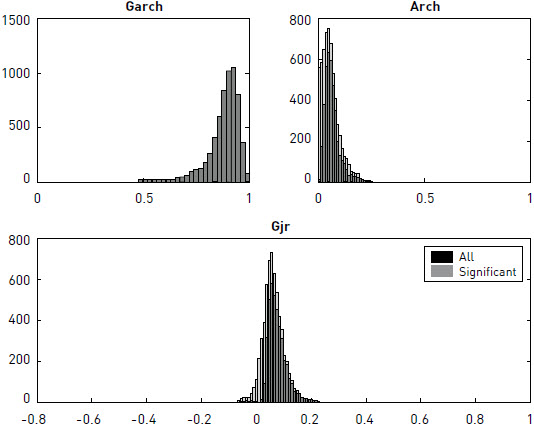

Appendix 3. Frequencies of ARCH, GARCH and GJR coefficients

This figure displays the distribution of the GARCH term (upper left panel), of the ARCH term (upper right panel) and of the asymmetry parameter of the GJR model (lower panel). All coefficients are displayed.

Appendix 4. Summary statistics of the estimated coefficients

This table summarizes the estimates of the ARCH (α), GARCH (β), GJR (γ) - the asymmetry parameter of the GJR model and T-statistics of the Dynamic Quantile test for Short and Long position.

Biographical notes

Jean-Laurent Viviani is professor of Finance at University Rennes 1. He is head of the master “Cash Management” at IGR IAE Rennes and co-head of the chair “New challenges for banks: Social responsibility, efficiency and risks”. His researches are focused on the financing of supply chain, the risks and the banking governance, the Corporate Social Responsibility and the financial decisions under uncertainty.

Malick Fall is lecturer in Finance at University Rennes 1. His researches are mainly quantitative and involve financial markets as well as corporate finance.

Christophe Revelli is associate professor of responsible finance and head of the MSc Corporate and Sustainable Finance at Kedge Business School. He is also board member at French Social Investment Forum (French SIF). His courses and researches are focused in the field of responsible finance, of the critical approach of the modern financial theory and of impact investing.

Notes

-

[1]

We consider predictability (Goodwin & Wright, 2010) as the capability of forecasters to produce a well-calibrated probability distribution. Perfect calibration would be achieved, for example, if it is observed that stock returns are higher than the VaR99%, 1% of the days.

-

[2]

Our results of course depends on the time series model we used (classical GARCH and GJR model). It could be the case that SR ratings be useful in predicting risk if risk managers use other risk prediction models.

-

[3]

The emergence of the French SRI and TEEC Labels could be good examples of SR investors engaged in sustainable development asset management strategies and favoring the development of SR companies from economic and market point of views.

-

[4]

To illustrate, we can take the example of electric and classical carmakers that could have similar volatilities (being in the same industry…) but the upside potential of electric could probably be higher (so the kurtosis).

-

[5]

There is a debate on the impact of idiosyncratic risk on expected return since the seminal paper of Goyal and Santa-Clara (2003).

-

[6]

Kinder, Lydenberg, Domini Research & Analytics (today owned by MSCI ESG Research).

-

[7]

A violation occurs when the returns are lower (higher) than VaR for the long position (short position).

-

[8]

A merger between Vigeo and EIRIS (English social rating agency) was approved in October 2015 to form the Vigeo-EIRIS group.

-

[9]

The different criteria evaluated by Vigeo to establish the social ratings are explained in Appendix 1.

-

[10]

Equation (11) (fixed effect model) is a simplified version of the conditional fixed effect model that we actually used in our empirical work. The choice of the conditional model is justified to take into account identification problems.

-

[11]

The distribution of the ARCH, GARCH and Asymmetric (GJR) coefficients are given in Appendix 3. Summary statistics of the estimated coefficients are given in Appendix 4.

-

[12]

As a robustness check, we conduct a similar empirical analysis on a sample where we suppose that the Vigeo ratings remains valid two years after its first computation unless another rating was calculated during this period. In this case, we also find that HR (Human Resources) has a significant positive effect on the GARCH coefficient.

Bibliography

- Arvidsson, Adam (2009). “The Ethical Economy: Towards a Post-Capitalist Theory of Value”, Capital and Class, Vol. 33, N° 1, p. 13-29.

- Aupperle, Kenneth E.; Carroll, Archie B.; Hatfield, John D. (1985). “An Empirical Examination of the Relationship between Corporate Social Responsibility and Profitability”, Academy of Management Journal, Vol. 28, N° 2, p. 446-463.

- Beltratti, Andrea (2003). “Socially Responsible Investment in General Equilibrium”, Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=467240.

- Benlemlih, Mohammed; Girerd-Potin, Isabelle (2014). “Does Corporate Social Responsibility Affect Firm Financial Risk? Evidence from Vigeo Data”, Paper presented at the meeting of the International French Finance Association (AFFI), Aix en Provence.

- Black, Fischer (1976). “Studies of stock price volatility changes”, Proceedings of the Business and Economics Section of the American Statistical Association, p. 177-181.

- Bouslah, Kais; Kryzanowski, Lawrence; M’zali, Bouchra (2013). “The impact of the dimensions of social performance on firm risk”, Journal of Banking and Finance, Vol. 37, p. 1258-1273.

- Boutin-Dufresne, François; Savaria, Patrick (2004). “Corporate social responsibility and financial risk”. The Journal of Investing, Vol. 13 (spring), p. 57-66.

- Choi, Tae H., Pae, Jinhan (2011). “Business Ethics and Financial Reporting Quality: Evidence from Korea”, Journal of Business Ethics, Vol. 103, N° 3, p. 403-427.

- Christoffersen, Peter F. (1998). “Evaluating interval forecasts”, International Economic Review, Vol. 39, N° 4, p. 841-862.

- Doornik, Jurgen A. (2007). Object-oriented matrix programming using Ox, 3rd Ed, London, Timberlake Consultants Press and Oxford.

- Dumitrescu, Elena-I.; Hurlin, Christophe; Pham, Vinson (2012). “Backtesting value-at-risk: From dynamic quantile to dynamic binary tests”. Finance, Vol. 1, N° 33, p. 79-112.

- Dupre, Denis; Girerd-Potin, Isabelle; Jimenez-Garces, Sonia; Louvet, Pascal (2009). “Influence de la notation éthique sur l’évolution du prix des actions”. Revue Economique, Vol. 60, N° 1, p. 5-31.

- Engle, Robert F.; Manganelli, Simone (2004). “CAViaR: Conditional autoregressive value-at-risk by regression quantiles”, Journal of Business and Economic Statistics, Vol. 22, N° 4, p. 367-381.

- Friedman, Milton (1970). “The social responsibility of business is to increase profits”. New York Times, September 13, p. 122-126.

- Fombrun, Charles J.; GARDBERG, Naomi A.; BARNETT, Michael L. (2000). “Opportunity platforms and safety nets: Corporate citizenship and reputational risk”, Business and Society Review, Vol. 105, p. 85-106.

- Freeman, Robert E. (1984). Strategic management: A stakeholder approach, Boston, M.A Pitman.

- Giot, Pierre; Laurent, Sébastien (2003). “Value at risk for long and short trading positions”, Journal of Applied Econometrics, Vol. 18, N° 6, p. 641-663.

- Girerd-Potin, Isabelle; Jimenez-Garces, Sonia; Louvet, Pascal (2014). “Which Dimensions of Social Responsibility Concern Financial Investors?”, Journal of Business Ethics, Vol. 121, N° 4, p. 559-576.

- Godfrey, Paul C. (2005). “The relationship between corporate philanthropy and shareholder wealth: a risk management perspective”, Academy of Management Review, Vol. 30, N° 4, p. 777-798.

- Goodwin, Paul; Wright, George (2010). “The limits of forecasting methods in anticipating rare events”, Technological Forecasting & Social Change, Vol. 77, p. 355-368.

- Goyal, Amit; Santa-Clara, Pedro (2003). “Idiosyncratic Risk Matters!”, Journal of Finance, Vol. 58, N° 3, p. 975-1007.

- Hemingway, Christine A.; Maclagan, Patrick W. (2004). “Managers’ personal values as drivers of corporate social responsibility”, Journal of Business Ethics, Vol. 50, N° 1, p. 33-44.

- Humphrey, Jacquelyn E.; Lee, Darren D.; Shen, Yaokan (2012). “Does it cost to be sustainable?”, Journal of Corporate Finance, Vol. 18, N° 3, p. 626-639.

- Jensen, Michael C. (2001). “Value maximization, stakeholder theory, and the corporate objective function”, Journal of Applied Corporate Finance, Vol. 14, N° 3, p. 8-21.

- Jin, Li; Meyers, Stewart C. (2006). “R2 around the world: New theory and new tests”, Journal of Financial Economics, Vol. 79, N° 2, p. 257-292.

- Jo, Hoje; NA, Haejung (2012). “Does CSR reduce firm risk? Evidence from controversial industry sectors”, Journal of Business Ethics, Vol. 110, N° 4, p. 441-457.

- Kim, Jim-Woo (2010). “Assessing the long-term financial performance of ethical companies”, Journal of Targeting, Measurement and Analysis for Marketing, Vol. 18, p. 199-208.

- Kim, Yongtae; Li, Haidan; Li, Siqi (2014). “Corporate social responsibility and stock price crash risk”, Journal of Banking and Finance, Vol. 43, p. 1-13.

- Kurtz, Lloyd (2002). “Studies in the field of SRI investing”, Working paper, www.sristudies.org.

- Kytle, Beth; Ruggie, John G. (2005). “Corporate social responsibility as risk management: A model for multinationals”. Working paper, Harvard University.

- Lahrech, Houssam (2011). “Disarming the value killers: CSR viewed through a sharp risk management lens”, Working paper, University of Nottingham.

- Laurent, Sébastien; Peters, Jean-Philippe (2002). “G@rch 2.2: An Ox Package for Estimating and Forecasting Various ARCH Models”, Journal of Economic Surveys, Vol. 16, N° 3, p. 447-485.

- Liang, Hao; Renneboog, Luc (2017). “On the foundations of corporate social responsibility”, Journal of Finance, Vol. 72, N° 2, p. 853-910.

- Mcguire, Jean B.; Sundgren, Alison; Schneeweis, Thomas (1988). “Corporate social responsibility and firm financial performance”, Academy of Management Journal, Vol. 31; N° 4, p. 854-872.

- McWilliams, Abagail; Siegel, Donald (2001). “Corporate social responsibility: A theory of the firm perspective”, Academy of Management Review, Vol. 26, N° 1, p. 117-127.

- Martínez-Ferrero, Jennifer; Garcia-Sanchez, Isabel; Cuadrado-Ballesteros, Beatriz (2015). “Effect of Financial Reporting Quality on Sustainability Information Disclosure”, Corporate Social Responsibility and Environmental Management, Vol. 22, N° 1, p. 45-64.

- Mishra, Saurabh; Modi, Sachin B. (2013). “Positive and negative corporate social responsibility, financial leverage, and idiosyncratic risk”, Journal of Business Ethics, Vol. 117; N° 2, p. 431-448.

- Nofsinger, John; Varma, Abhishek (2014). “Socially responsible funds and market crises”, Journal of Banking & Finance, Vol. 48, p. 180-93.

- Oikonomou, Ioannis; Brooks, Chris; Pavelin, Stephen (2012). “The impact of corporate social performance on financial risk and utility: A longitudinal analysis”, Financial Management, Vol. 41, N° 2, p. 483-515.

- Orlitzky, Marc; Benjamin, John D. (2001). “Corporate social performance and firm risk: A meta-analytic review”, Business and Society, Vol. 40, p. 369-396.

- Porter, Michael E. (1991). “American‘s Green Strategy”. Scientific American, Vol. 264, N°4.

- Preston, Lee E.; O‘Bannon, Douglas P. (1997). “The Corporate Social – Financial Performance Relationship: A Typology and Analysis”, Business and Society, Vol. 36, N° 4, p. 419-429.

- PRIOR, Diego; Surroca, Jordi; Tribo, Josep A. (2008). “Are socially responsible managers really ethical? Exploring the relationship between earnings management and corporate social responsibility”, Corporate Governance, Vol. 16, N° 3, p. 160-177.

- Quéré, Bertrand P.; Nouyrigat, Geneviève; Baker, Richard C. (2018). “A Bi-Directional Examination of the Relationship between Corporate Social Responsibility Ratings and Company Financial Performance in the European Context”, Journal of Business Ethics, Vol. 148, N° 3, p.527-544.

- Salama, Aly; Anderson, Keith; Toms, Steve (2011). “Does community and environmental responsibility affect firm risk? Evidence from UK Panel Data 1994-2006”, Business Ethics: A European Review, Vol. 20, N° 2, p. 192-204.

- Scholtens, Bert; Zhou, Yangqin (2008). “Stakeholder relations and financial performance. Sustainable Development”, Vol. 16, p. 213-232.

- Windsor, Duane. (2006). “Corporate Social Responsibility: Three key approaches”, Journal of Management Studies, Vol. 43, N° 1, p. 93-114

- Zahra, Shaker A.; Priem, Richard L.; Rasheed, Abdul A. (2005). “The antecedents and consequences of top management fraud”, Journal of Management, Vol. 31, N° 6, p. 803-828.

Appendices

Notes biographiques

Jean-Laurent Viviani est professeur de finance à l’Université de Rennes 1. Il est responsable du master Finance parcours “Trésorerie” à l’IGR IAE Rennes et co-directeur de la chaire “Nouveaux défis de la banque : Responsabilité sociétale, Efficience et Risques”. Ses recherches actuelles portent sur le financement de la chaîne logistique, les risques et la gouvernance bancaire, la Responsabilité Sociale de l’Entreprise et les décisions financières en incertitude.

Malick Fall est maître de conférence en Finance à l’Université de Rennes 1. Ses recherches sont principalement quantitatives et portent autant sur la Finance de Marché que sur la Finance d’Entreprise.

Christophe Revelli est professeur associé de finance responsable et directeur académique du MSc Corporate and Sustainable Finance de Kedge Business School. Il est également administrateur au Forum pour l’Investissement Responsable (FIR, French SIF). Ses cours et ses recherches s’inscrivent dans le champ de la finance responsable, de l’approche critique de la théorie financière moderne et de l’impact investing.

Appendices

Notas biograficas

Jean-Laurent Viviani es profesor de finanzas en la Universidad de Rennes 1. Está a cargo del master curso de finanzas “Tesorería” en el IGR IAE Rennes y codirector de la cátedra “Nuevos desafíos del banco: responsabilidad social, eficiencia y riesgos”. Su investigación actual se centra en las finanzas de la cadena de suministro, los riesgos y la gobernanza bancaria, la responsabilidad social de las empresas y las decisiones financieras en la incertidumbre.

Malick Fall es profesor de finanzas en la Universidad de Rennes 1. Su investigación es principalmente cuantitativa y se centra tanto en las finanzas de mercado como en las finanzas corporativas.

Christophe Revelli es profesor asociado de finanzas responsables y director académico del Master de Corporate and Sustainable Finance en Kedge Business School. También es administrador en el French Social Investment Forum (French SIF). Sus cursos e investigaciones están en el campo de las finanzas responsables, el enfoque crítico de la teoría financiera moderna y la inversión de impacto.

List of figures

FIGURE 1

Evolution of median Vigeo SR scores for each SR dimension

FIGURE 2

Comparison of the GARCH and GJR time series models in the case of long and short portfolios

This figure displays the distribution of the GARCH term (upper left panel), of the ARCH term (upper right panel) and of the asymmetry parameter of the GJR model (lower panel). All coefficients are displayed.

List of tables

Table 1a

Summary statistics of Vigeo’s SR scores

This table summarizes the six Vigeo scores (Environment (ENV), Corporate Governance (CG), Human Rights at workplaces (HRTS), Human Resources (HR), Business Behaviour (BB) and Community Involvement (CIN). MV and Leverage refer respectively to the ‘log of market capitalization’ and the ‘ratio of debt over total assets’.

Table 1b

Summary statistics: distribution of the sample by years and countries

Table 2

SR scores and market risk characteristics: Fixed effect panel data model

Table 2 (continuation)

* p < 0.10, ** p < 0.05, *** p < 0.01.

r2, r2(b) and r2(o) denote, respectively, the within, between and overall r-squared. F is Fischer statistic and Su and Se are respectively the panel-level standard deviation and standard deviation of vit. N, Ng, Min, Avg and Max refer, respectively, to the total number of observations, the total number of groups, the minimum, average and maximum number of groups. The dependent variables N-VaR, P-VaR, GJR, ARCH, GARCH, () and E(r) refer respectively to the negative empirical VaR, positive Empirical VaR, the asymmetry parameter of the GJR model, the ARCH coefficient, the GARCH coefficient, the (daily) variance and the (daily) average returns. T-statistics are given in parentheses. LL is the log-likelihood. Standard errors are cluster–robust standard errors.

Table 3

SR scores and market risk predictability: Conditional fixed-effects logit model

* p < 0.10, ** p < 0.05, *** p < 0.01.

N, Ng , Min, Avg and Max refer, respectively, to the total number of observations, the total number of groups, the minimum, average and maximum number of groups. A large number of groups has been dropped because some groups have the same dependent variable (vector with only one or zero values) whereas the estimation required at least two different outcomes. Chi2 and LL are respectively the statistic of the chi2 test and the log-likelihood of the model. t statistics are given in parentheses. The dependent variables DQT(GARCH) SHORT and DQT(GJR) LONG are binaries variable that indicate success (1) or failure (0) of the null of adequate VaR modelling based on the DQT test using results of the GARCH models for short position VaR and of the GJR model for the long position VaR (found to be the most appropriate model for each position).

This table displays results of the Hausman test applied on the regression presented in table 2. The Hausman test has for null hypothesis that the random effect model should be preferred, p-values are below 0.01 indicating that the alternative, the fixed effect model should be employed.

This table summarizes the estimates of the ARCH (α), GARCH (β), GJR (γ) - the asymmetry parameter of the GJR model and T-statistics of the Dynamic Quantile test for Short and Long position.